The Spanish dermocosmetics market continues to attract strong investor interest, supported by resilient category growth, premium positioning and favourable consumer trends. Yet many evaluation frameworks still underemphasise one of the most important drivers of long-term value creation: channel positioning.

While brands increasingly operate across multiple routes to market, channel strategy remains central to competitive advantage, shaping pricing discipline, consumer trust, recommendation dynamics and margin resilience. As the market becomes more crowded and omnichannel expansion accelerates, the ability to manage channel architecture effectively is emerging as a critical differentiator between high-quality assets and average transactions.

The Spanish skincare market grew at approximately 7% annually between 2022 and 2025, outpacing the broader beauty and personal care sector, and is forecast to sustain c.4%-5% annual growth through 2030. Ecommerce remains the fastest-growing channel at c.12% annually, while pharmacies continue to represent c.15%-20% of the market, reflecting their enduring role in recommendation-led purchasing.

Three developments are reshaping competitive dynamics across the category.

First, the “skincare as healthcare” trend has broadened the consumer base well beyond traditional pharmacy shoppers. Younger consumers are entering the category through digital channels with high ingredient literacy and strong exposure to influencer-led discovery.

Second, the competitive landscape has become increasingly fragmented. Pharmacy shelves once dominated by a limited number of established brands now face competition from a growing number of credible local and international players.

Third, and most importantly for investors, channel conflict has become a defining strategic challenge. Brands that expanded distribution without preserving pricing discipline or channel differentiation have, in some cases, weakened pharmacist recommendation rates and undermined brand credibility.

Channel positioning shapes long-term value

Many investors continue to prioritise brand equity over the economics of the channels through which that equity is monetised. However, channel architecture increasingly determines the sustainability of growth, pricing power and competitive defensibility.

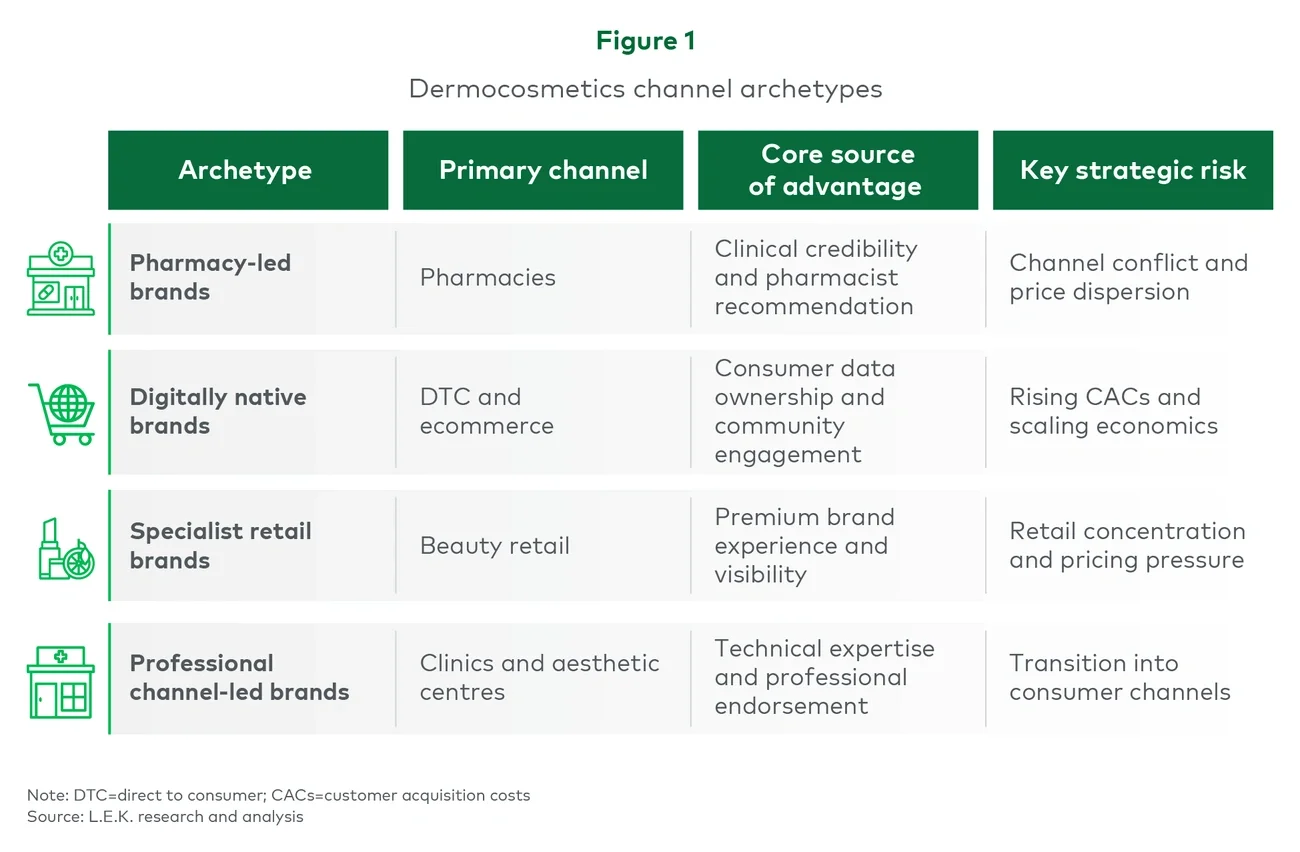

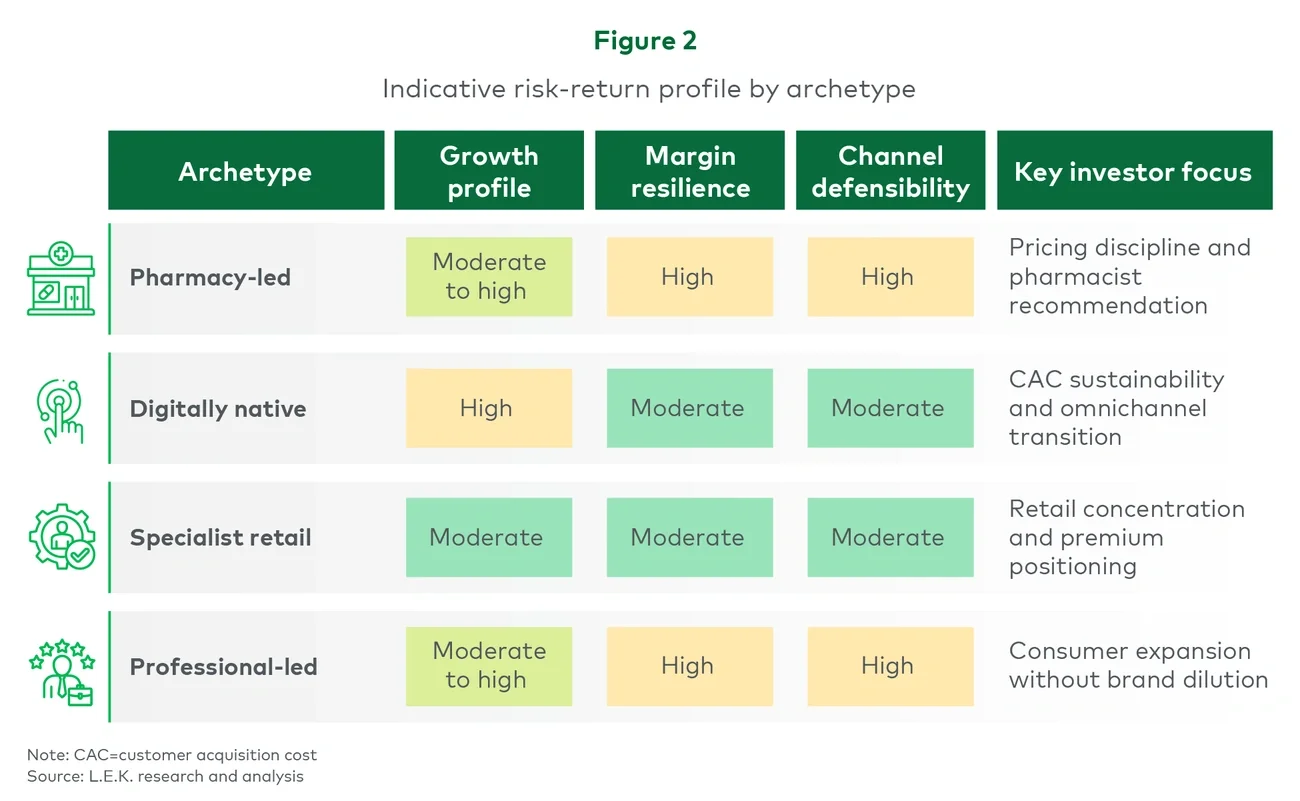

Four broad archetypes continue to define the Spanish dermocosmetics landscape. While the boundaries between them are becoming less distinct, each structural characteristic is rooted in its original channel strategy (see Figure 1).