Key takeaways

-

The highly fragmented chemical distribution sector has seen a flurry of merger and acquisition activity in the past five years, with no slowdown in sight.

-

Thanks to the increased use of distributors, growth projections for this sector have ramped up beyond those of the chemical end market as a whole.

-

Specialty chemicals enjoy an even more robust growth projection.

-

Most companies looking for attractive additions to their portfolio of chemical distributors are pursuing one of three expansion paths: geographic, product or end market.

Big opportunities await buyers that are looking for deals in the chemical distribution sector right now. Dramatic shifts in the $470 billion U.S. chemical industry, particularly in the highly fragmented distribution sector, have set off a flurry of mergers and acquisitions (M&As) — with the top 10 distributors seeing more than 40 mergers in the past five years alone.

There is no slowdown in sight, particularly in the specialty chemicals segment, which has seen a steady uptick in M&A activity of late. L.E.K. Consulting expects this enthusiasm to continue for at least the next five years, as buyers search for more innovative ways to serve their clients and investors seek to broaden or deepen their portfolios.

The following analysis is part of our ongoing Executive Insights series on emerging trends and growth opportunities for U.S. chemical companies. In this installment, we take a look at the factors that make chemical distributors attractive candidates for M&A in the short and medium term: the critical role they play in the supply chain, the growing specialty chemicals subsector and the industry’s high level of fragmentation, all underscored by rosy growth projections. We also discuss the objectives, advantages and challenges of the three strategic paths dealmakers are most likely to negotiate on their road to acquisition activity: geographic, product and end market.

The allure of chemical distributors

Why are chemical distributors such desirable candidates for M&A? Thanks to the increased use of distributors, growth projections for the distribution sector have ramped up beyond those of the chemical end market as a whole. In fact, the sector is forecast to grow an average of 4%-5% a year over the next five years. Beyond a healthy outlook, there are several other attributes that create the right chemistry between the distributors’ key stakeholders and the financial and strategic dealmakers:

Critical supply chain link. Chemical distributors are an integral part of the supply chain and serve two primary groups of customers: chemical manufacturers, which need help reaching smaller or more specialized customers, and the end customer that is looking for access to products and services. Within this space, distributors perform myriad value-added services that chemical manufacturers and end customers cannot or choose not to do, including transportation, repackaging bulk products into smaller quantities, reformatting products based on customer specifications, and providing just-in-time delivery and vendor-managed inventory.

An even more critical service chemical distributors provide is high-touch advice and application support to end customers that often have limited R&D and are asset-light. These services are particularly important for smaller end customers, including specialty chemicals manufacturers. Dealmakers are wise to bear in mind that nearly a quarter of all specialty chemicals are sourced through distributors — a penetration level that is expected to increase.

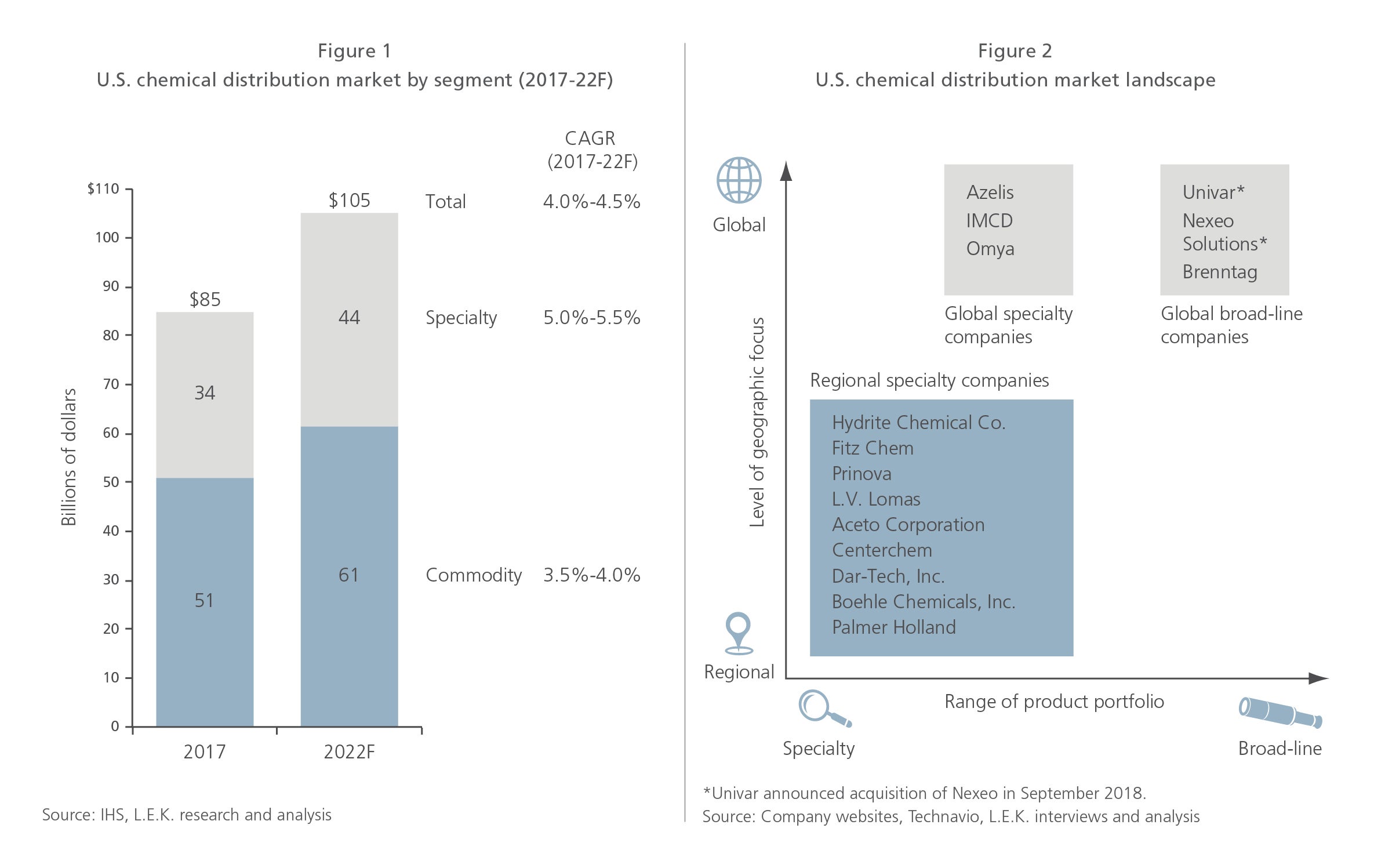

Specialty chemicals. Specialty chemicals enjoy an even more robust growth projection of 5.0%-5.5% (with more than 4.0%-4.5% growth expectations for the distribution sector) — a result of lower-volume customers and suppliers’ increasing use of specialty distributors to gain entry into new markets (see Figure 1). To top it off, specialty chemical distribution commands gross margins that are significantly higher than those of commodity chemicals — as much as 40% for complex chemicals such as pharmaceutical additives.

Fragmentation. Despite a trend toward consolidation, there are still more than 1,000 U.S. distributors active in the U.S. marketplace across both specialty and commodity products. The top two global players (Univar and Brenntag) hold only about 40% of the overall market, even after Univar’s recently announced acquisition of Nexeo. In specialty distribution, those same players command only 5%-10% of the market (see Figure 2). Recently, however, many broad-line distributors have begun turning their attention to specialty chemicals as a means of offering a wider range of products to both new and existing customers.

The paths more traveled

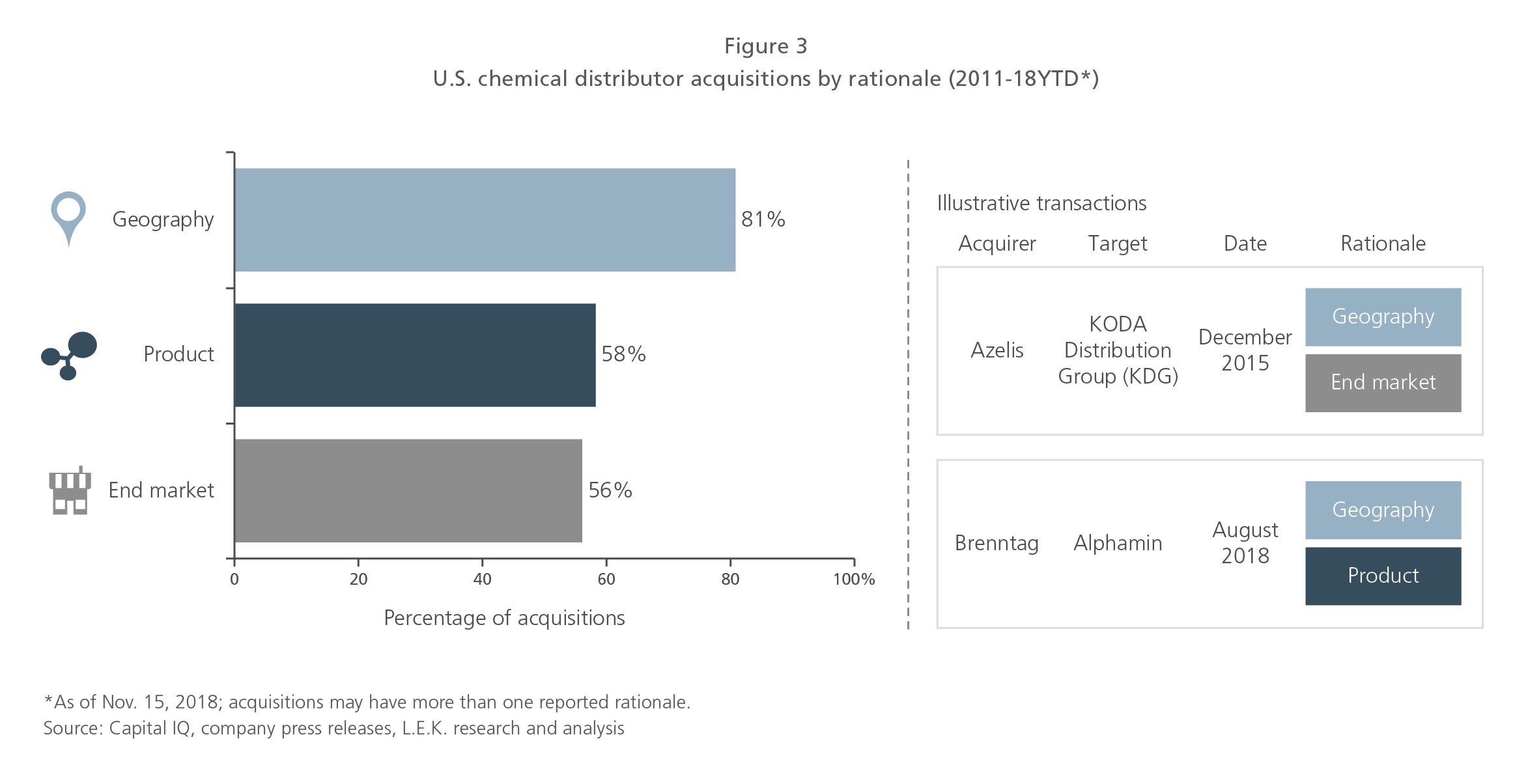

For dealmakers, then, the chemical distribution sector holds considerable appeal. Most companies looking for attractive additions to their portfolio of chemical distributors are pursuing one of three expansion paths: geographic, product or end market. To get a better handle on their acquisition objectives, we analyzed the press releases and deal terms of M&A transactions in the chemical distribution market between 2011 and November 2018. We then classified each transaction based on which strategy or strategies it exemplified (see Figure 3).

Each acquisition strategy has different objectives, advantages and challenges. Following is a more in-depth discussion of why buyers pursue each acquisition growth strategy and which attributes they value most in a target company.

Strategy 1: Geographic focus

Acquirers cited this strategy most frequently, viewing it as a way to rapidly achieve scale in underpenetrated areas and within a particular region, as well as to develop products tailored to customers in that region. This strategy can take one of several forms:

- Single brand, regional focus: Build a strong network that services customers in just one or two regions. This “big fish in a small pond” strategy is a way for smaller distributors to achieve greater market share within a specific region, which can both bolster their bargaining power with suppliers and create stickier customer relationships.

- Multiple brands, national presence: Consolidate multiple brands, each with a distinct regional footprint, to create a network with national coverage. This is a way for distributors to achieve national coverage without diluting their regional brands and at the same time limit conflicts between exclusivity contracts with chemical manufacturers.

- Single brand, national presence: Achieve broad national coverage under a single brand to gain greater leverage with suppliers and customers. This strategy allows distributors to build integrated logistics networks and achieve greater economies of scale, both of which can help them better serve certain customers.

In general, distributors with a well-defined rather than a general, geographic strategy are considered more desirable. For example, distributors pursuing a national presence with multiple brands may be especially attractive to foreign distributors that are looking for broader coverage in the U.S. and are less likely to run into supplier or customer conflicts. On the other hand, broad-line distributors seeking to fill specific geographic gaps in their network may be more interested in acquiring a company with a single-brand, regional focus.

Strategy 2: Product focus

A product-focused acquisition strategy aims to achieve scale and expertise in one or two specific product categories. Acquirers look for distributors with advanced technical expertise and a dedicated sales force, as it can be challenging to build these capabilities organically. They’re especially attracted to distributors that can handle the complex products that tend to be used in regulated industries such as food, pharmaceuticals, and (to some extent) personal care and beauty products. These markets command higher-than-average margins and have relatively steep barriers to entry. Finally, acquirers are on the hunt for distributors with sufficient scale to serve larger customers that need highly technical products.

A number of significant transactions over the past several years reflect a product-focused growth strategy. Consider TER GROUP, a leading European distributor, trader and producer of chemical raw materials, which acquired a 49% stake in Keim-Additec Surface USA LLC, the U.S. distributor of wax and silicone additives produced by parent company Keim-Additec Surface GmbH. This product category appealed to TER GROUP because it was seeking to expand into higher-value wax segments and to capitalize on increasingly stringent environmental regulations in coatings.

Strategy 3: End-market focus

An end-market-focused strategy makes sense when the market has a fragmented customer base and requires complex, differentiated products. Acquirers pursuing this strategy value targets with a full line of solutions that help them not only fill gaps in their own product lines but also achieve greater scale with existing customers in search of a broader range of products from a single distributor. Distributors with differentiated portfolios that are difficult to replicate are especially attractive. Also of interest are smaller distributors that have forged deep relationships with a well-delineated group of customers.

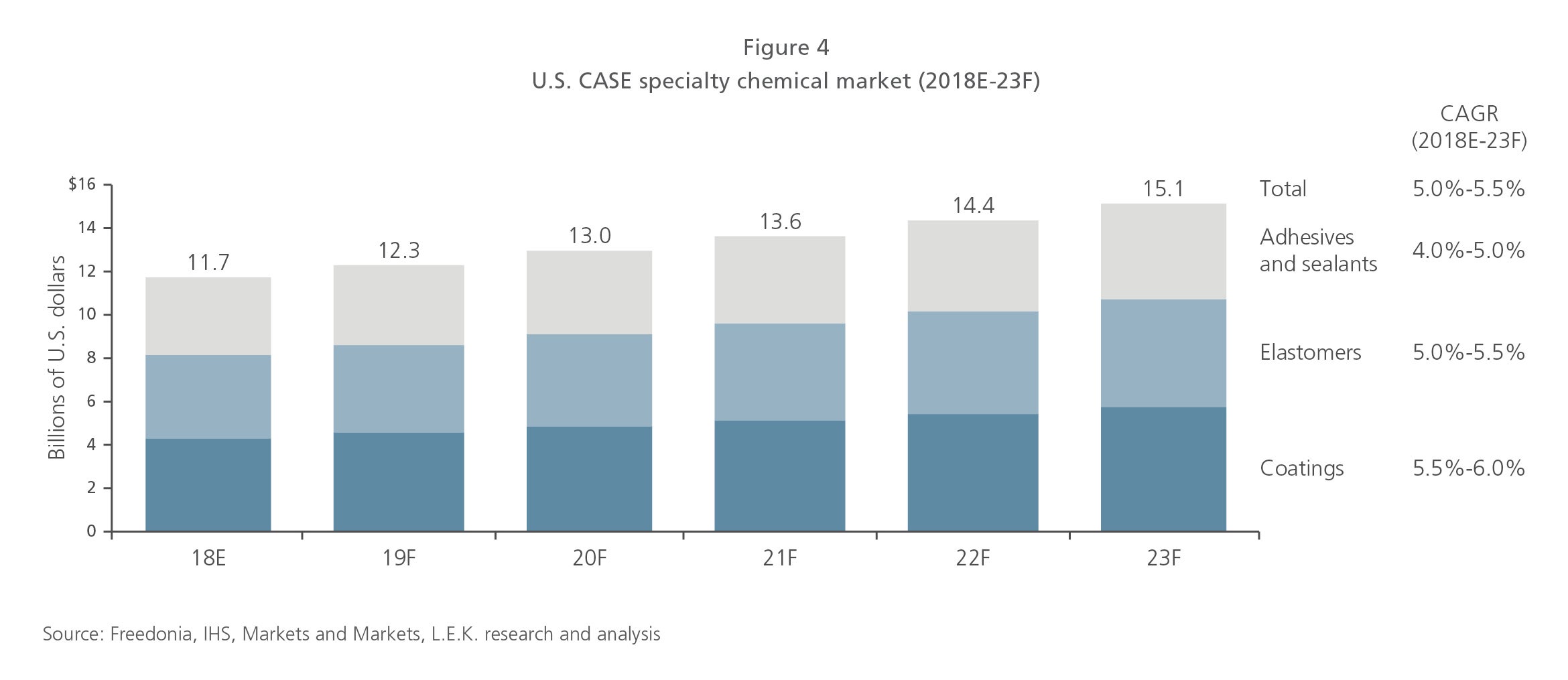

We believe several end markets will prove fertile hunting grounds for acquisitions, such as coatings, adhesives, sealants and elastomers (CASE). This end market enjoys higher margins than many other chemical end markets and has a higher barrier to entry due to its technical nature and regulated status. Moreover, the CASE sector includes a large number of smaller companies (those with less than $100 million in revenues) that are viable acquisition targets.

CASE products represent about $12 billion in sales, and nearly 40% of CASE products go through distributors, primarily because customers in this industry often require significant application support. Growth projections for CASE specialty chemicals are higher than those for the chemical industry in general, owing to several trends:

- Robust transportation and construction industries — both of which are primary users of CASE products (see Figure 4)

- Increased use of plastics in manufacturing

- A shift to more expensive “green” chemicals — the result of environmental regulations coupled with customer demand

Regardless of their strategic approach, buyers have abundant acquisition opportunities in the chemical distribution sector. The key is to identify target companies with the right fundamentals, in the most promising markets, whose capabilities and customers are an appropriate fit for the buyer. In other words, if the chemistry is right, the deal might be too.

05012019160557