COVID-19 in the US: Consumer Insights for Businesses — Edition 4, Part 1

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

In partnership with Civis Analytics, we’re publishing a series of insights on the consumer response to COVID-19. Our goal is to help our consumer-facing clients monitor sentiment and behaviors as they take shape during this unprecedented period.

At the same time, we acknowledge that the pandemic is a humanitarian crisis first and foremost. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this crisis.

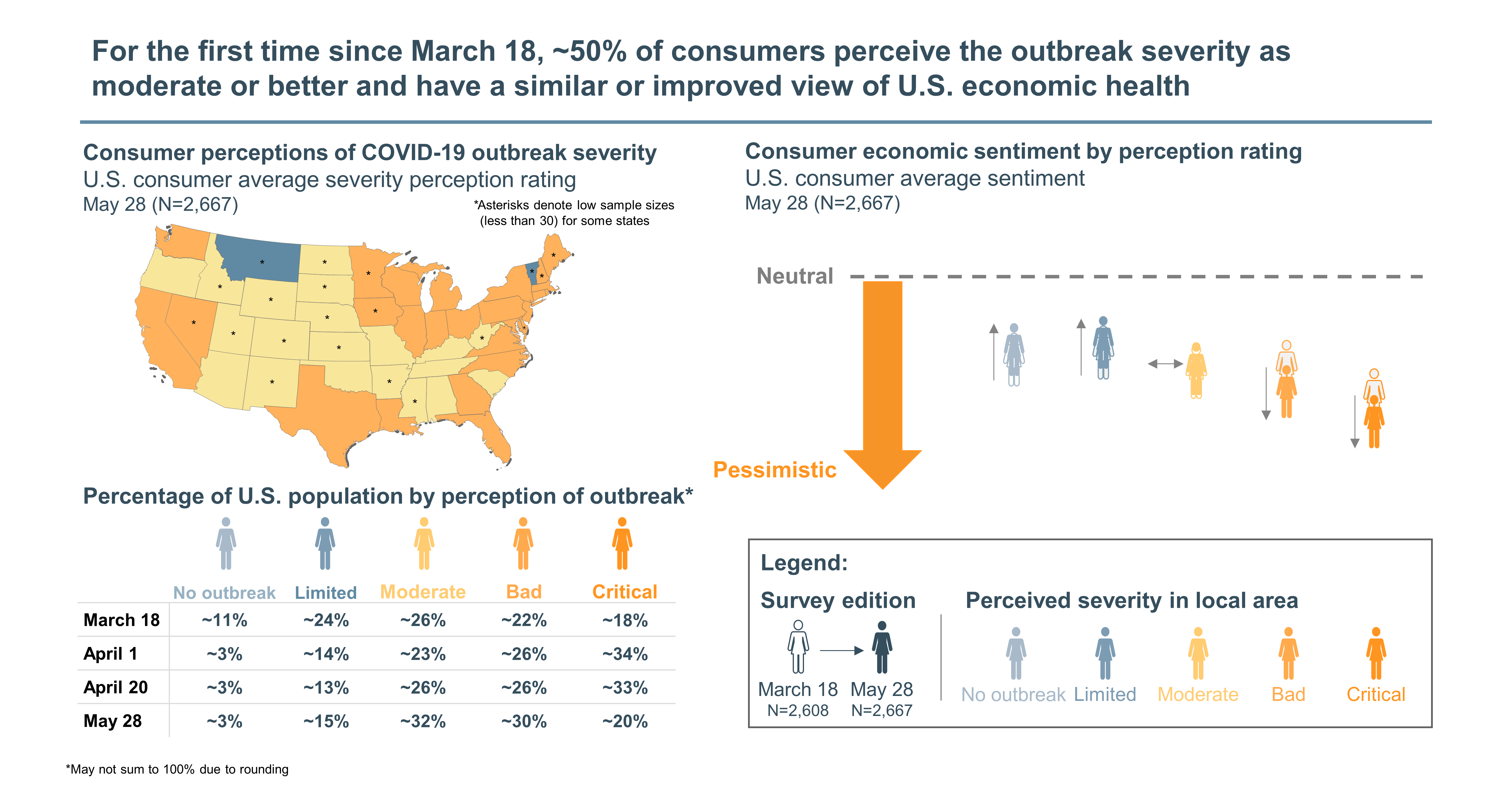

Consumer sentiment is significantly more positive than in the early stages of the outbreak. Economic sentiment is improving, with ~50% of consumers having a similar or slightly improved view of the U.S. economy (relative to March 18).

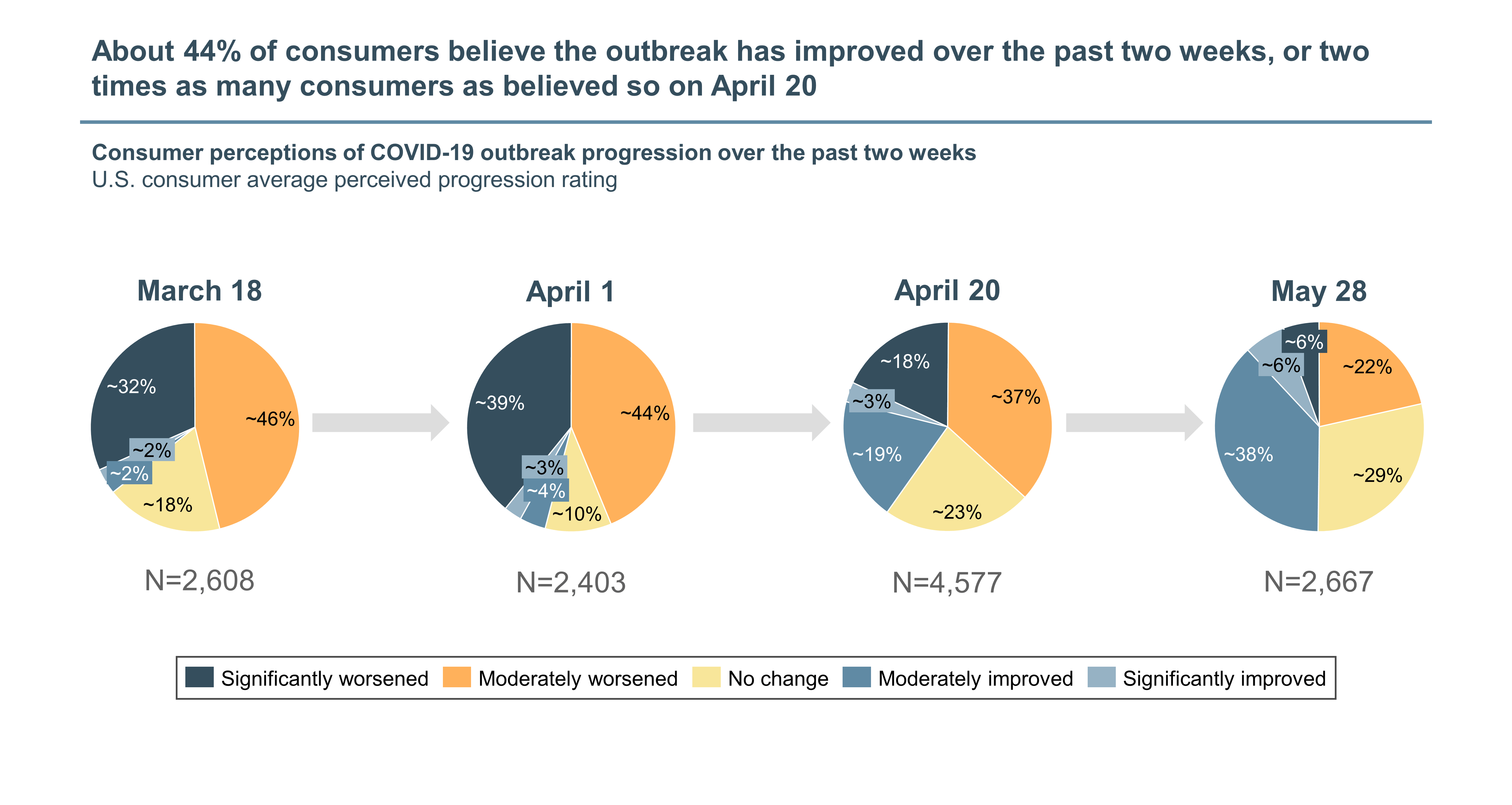

Approximately 44% of U.S. consumers believe the progression of the outbreak has improved in the past two weeks (up from ~22% on April 20 and ~4% on March 18).

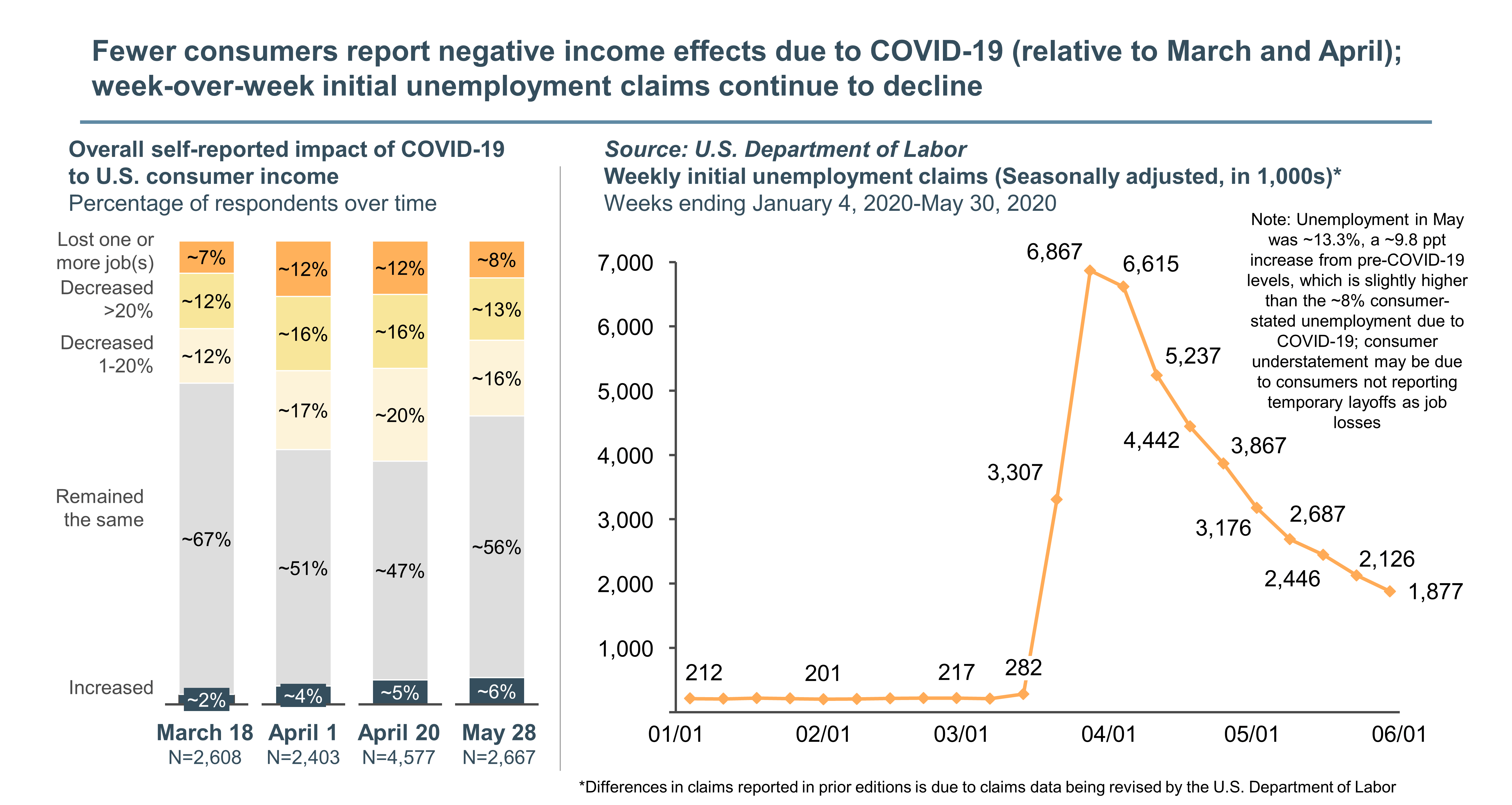

Encouragingly, the portion of consumers reporting a decline in income has decreased to ~37% (down from ~48% on April 20), likely driven by the increasing number of states that have loosened restrictions over the past month.

The total number of weekly initial unemployment claims continues to grow; however, fewer people are filing each week. Since the beginning of the outbreak, ~43 million Americans have filed initial unemployment claims, or ~27% of the labor force. However, the May unemployment rate was ~13.3% (down from the ~14.7% reported for April). This is ~9.8 ppt above pre-COVID-19 levels, which is slightly higher than consumer-stated unemployment of ~8% due to COVID-19. Consumer understatement may be due to consumers not reporting temporary layoffs as job losses.

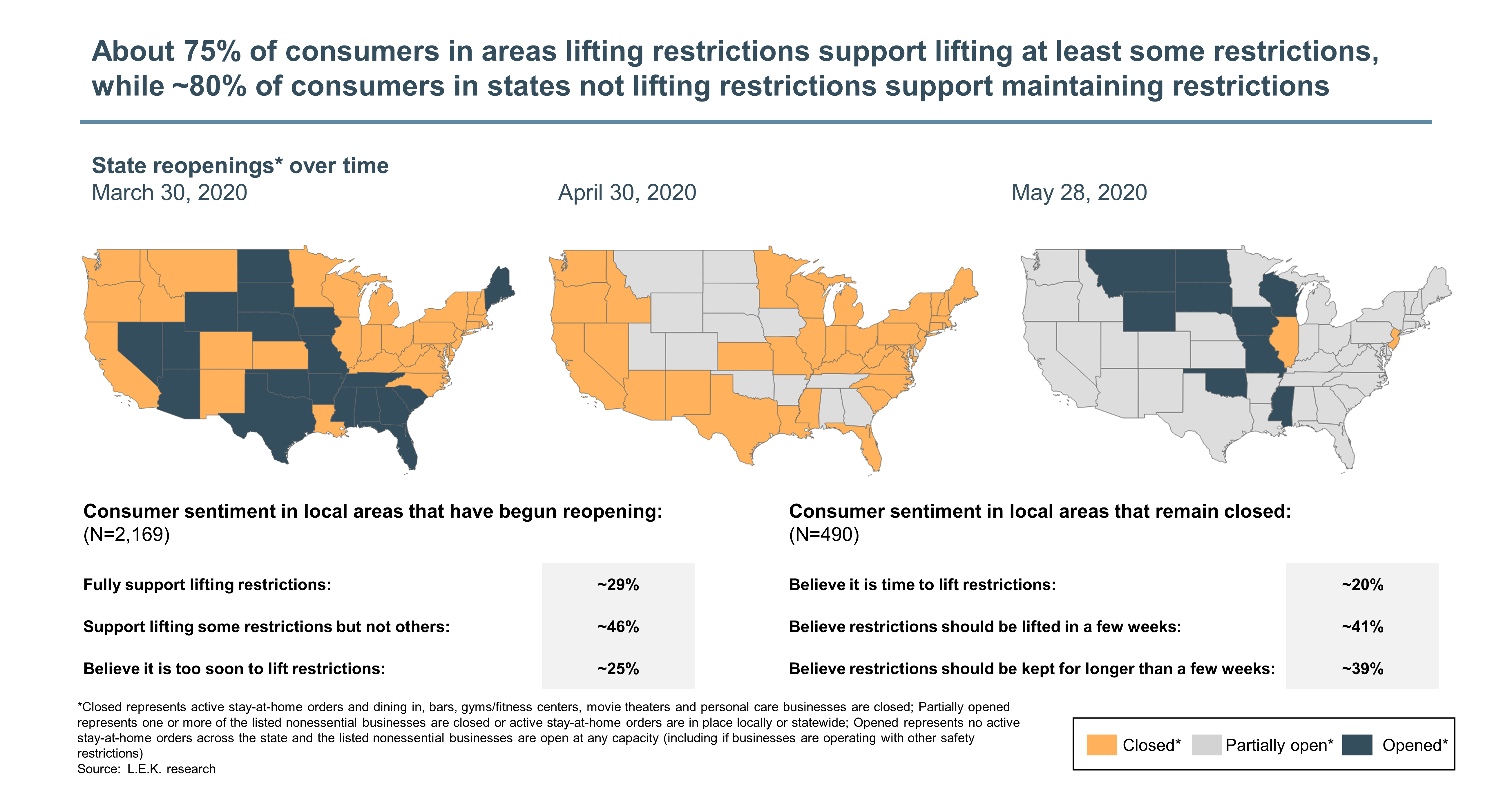

Within areas that have begun reopening, ~75% of consumers support lifting restrictions in some capacity. However, in areas that remain closed, ~80% of consumers support maintaining restrictions for at least the next few weeks.

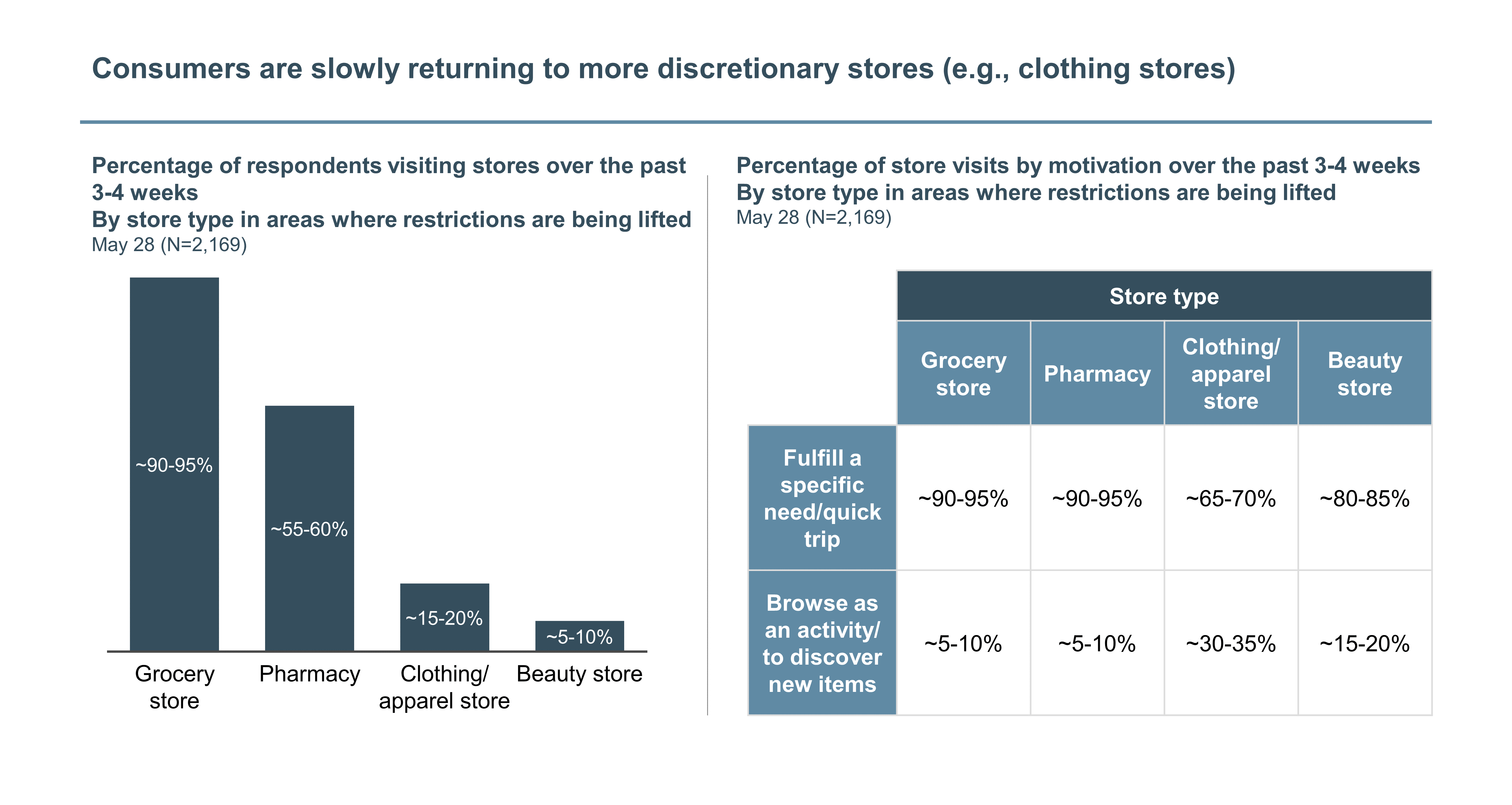

Consumers in areas that have begun lifting restrictions are slow to return to visiting stores. While store visits are high within nondiscretionary store types such as grocery and pharmacy, only ~15-20% of consumers indicated visiting a clothing/apparel store over the past three to four weeks. Even fewer (~5-10%) visited a beauty store. Consumers indicate that a significant majority of their store visits remain motivated by the need to pick up a specific item rather than to browse as an activity.

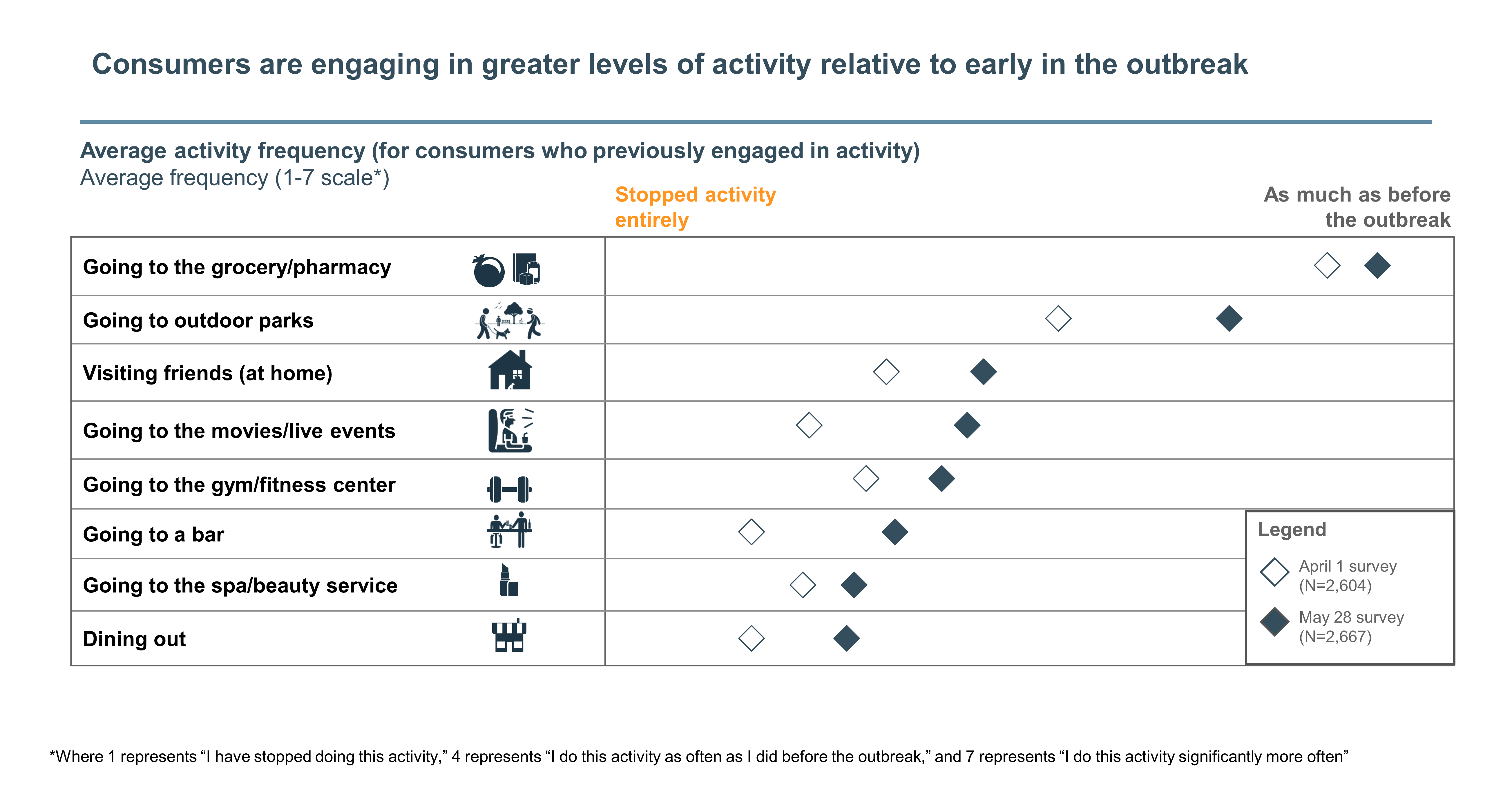

Consumer activity has increased relative to early outbreak levels across all activities tested. However, activity remains below pre-COVID-19 levels.

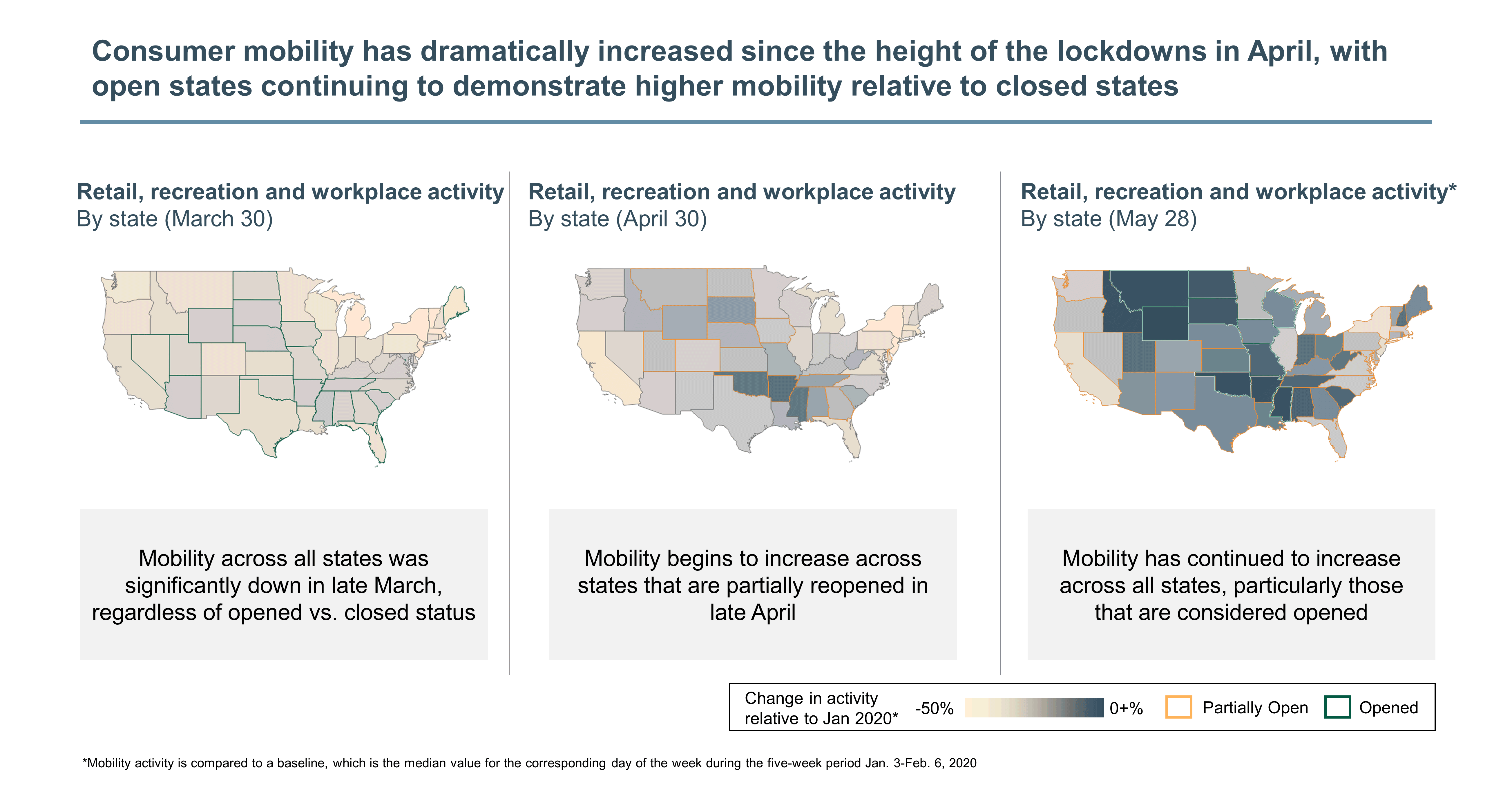

Google mobility data confirms an increase in activity for areas that are loosening restrictions. Retail, recreation and workplace mobility has significantly increased relative to levels in March and April, but generally remains below pre-COVID-19 levels. States that are open or partially open continue to demonstrate higher levels of activity relative to those that are not.

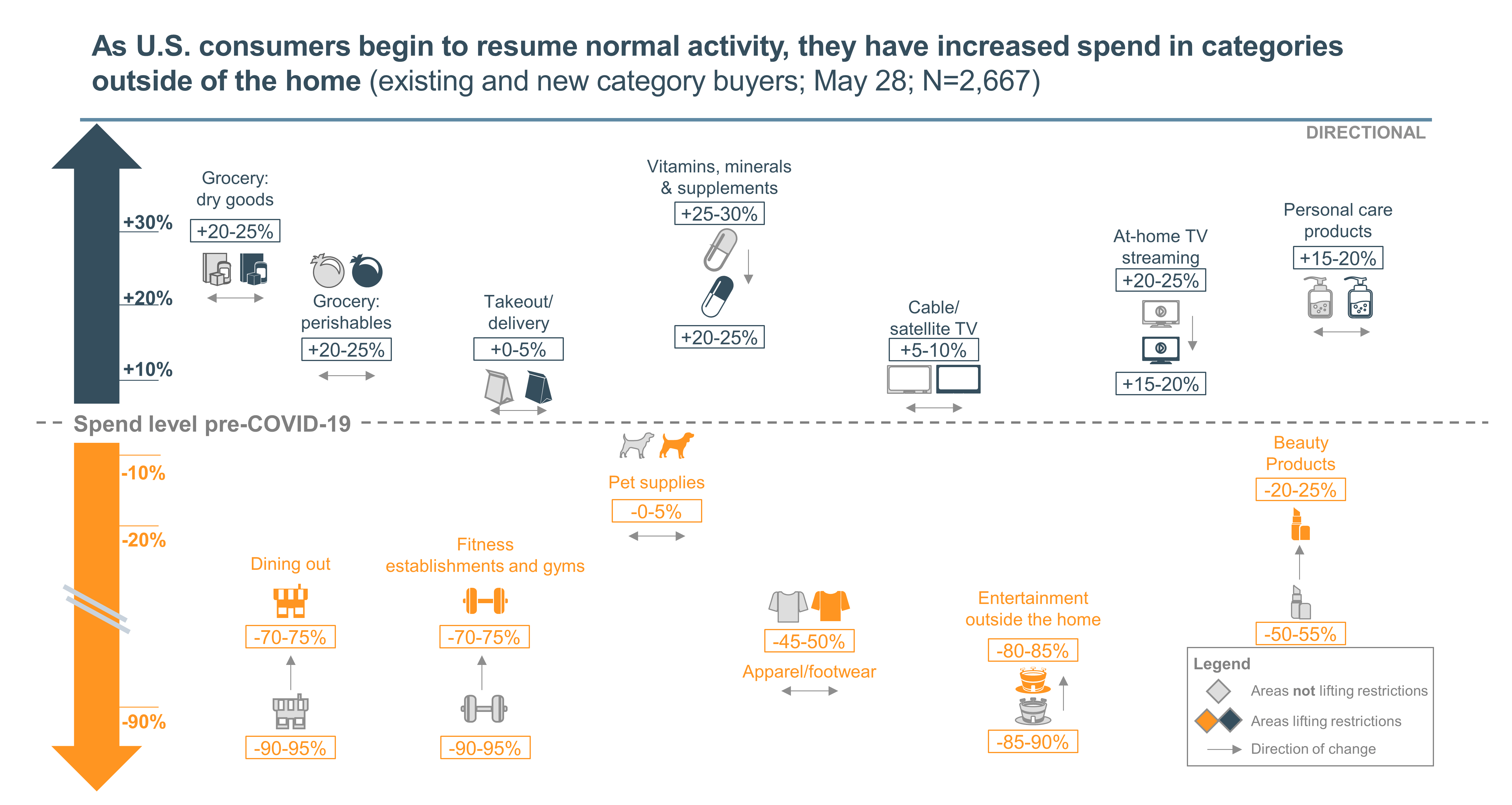

As states begin to lift restrictions, several product categories are seeing a change in spend relative to areas that are not lifting restrictions.

Spend is beginning to rebound in product categories that have been negatively impacted by the COVID-19 outbreak:

Some product categories experienced a decline in spend by consumers in areas lifting restrictions:

Television streaming experienced a decline as well, potentially due to consumers having more opportunities to engage in other recreational activities as states lift restrictions and weather continues to improve

Grocery spend is similar for consumers in areas lifting restrictions and areas not lifting restrictions. As states continue to reopen, this spend may begin to shift closer to pre-COVID-19 levels, with consumers looking to dine out more or increase spend in other discretionary areas.

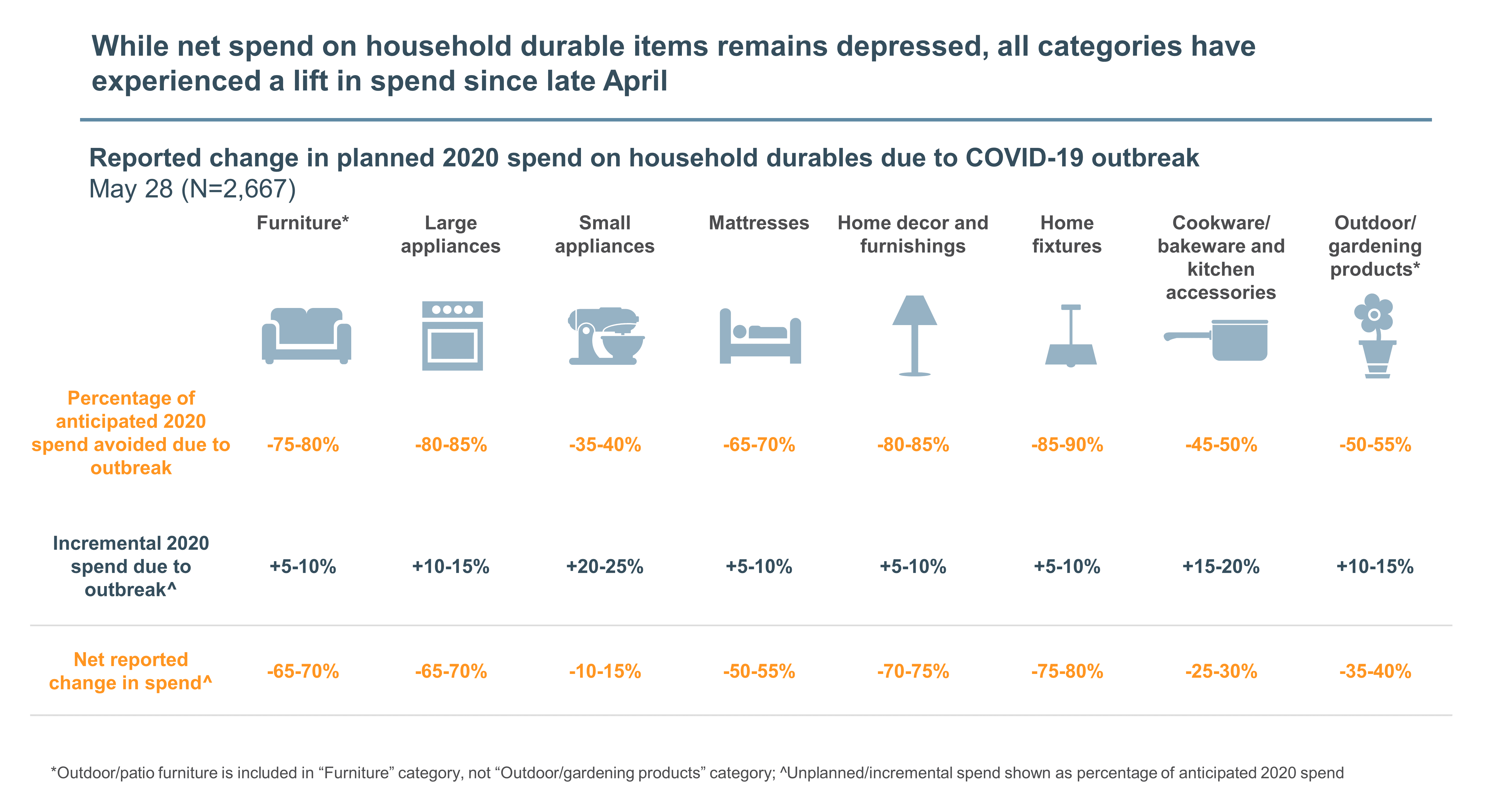

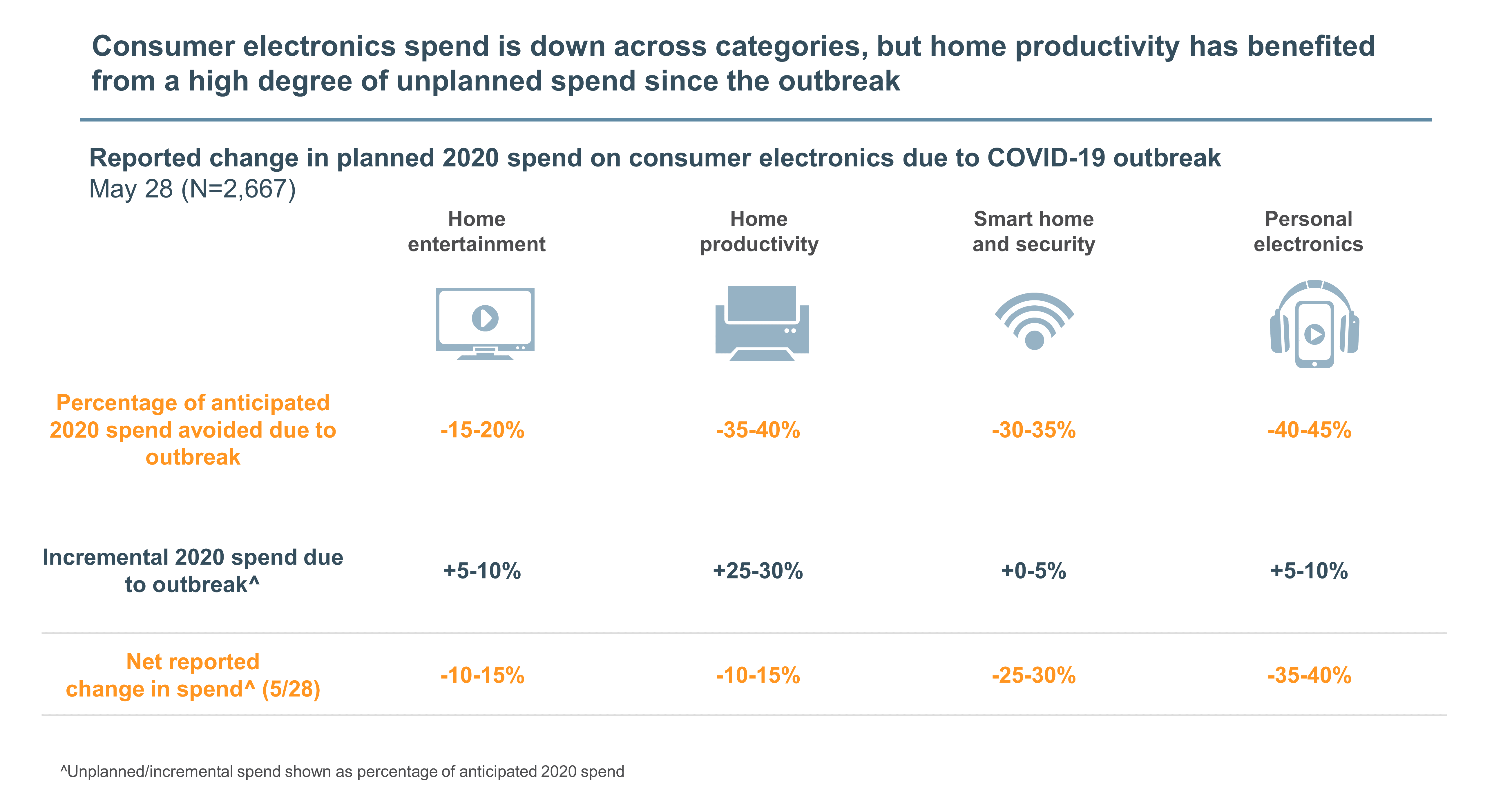

Consumers report that they plan to cancel or avoid a significant portion of anticipated spend during 2020 on household durables and consumer electronics subcategories (including any spend that has already been canceled or avoided).

However, as the outbreak has continued, consumers report high levels of unplanned spend in the following categories:

This unplanned spend has helped offset the steep declines in spend due to COVID-19. Still, consumer-reported spend indicates spend remains down across product categories relative to pre-COVID-19 levels.

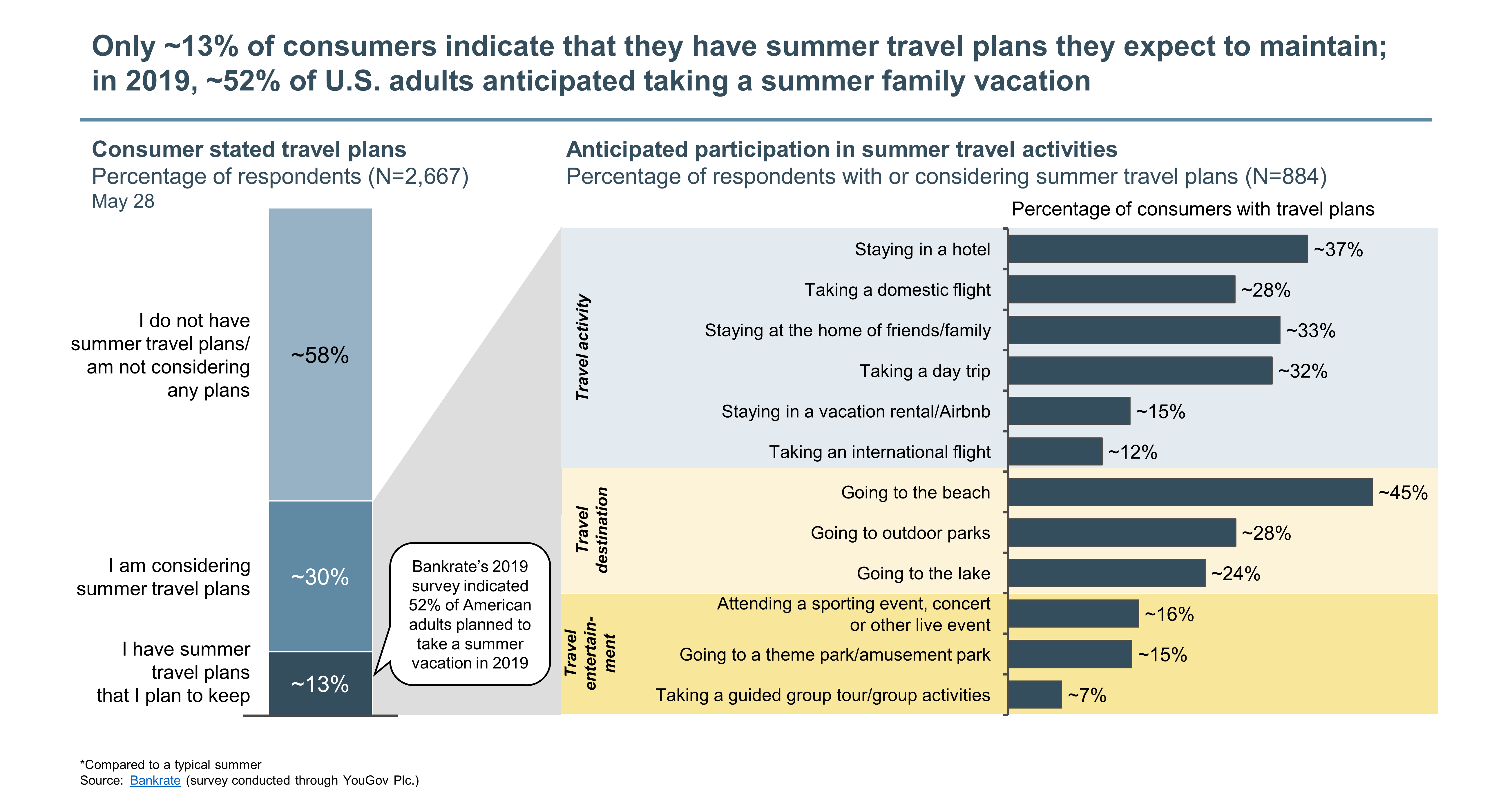

Only ~13% of consumers currently have summer travel plans they expect to keep, with another ~30% considering summer travel plans. For comparison, a March 2019 Bankrate survey stated that 52% of American adults planned to take a summer vacation in 2019.

Approximately 37% of consumers with or considering summer travel plans listed staying in a hotel as part of their plans, making it the most popular summer travel activity. Going to the beach is the most popular destination (~45%), and attending a live event is the most popular entertainment option (~16%).

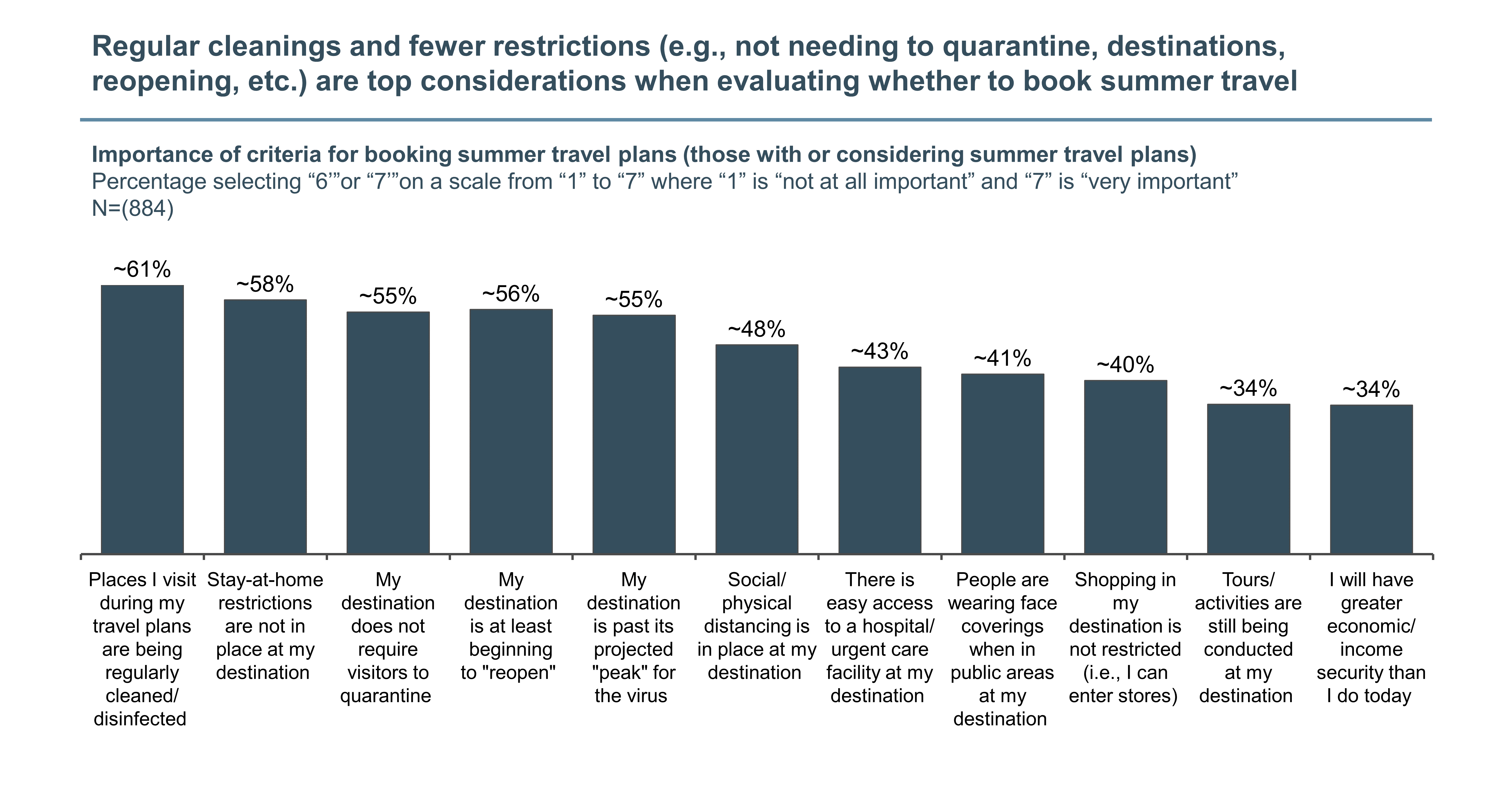

As consumers decide to book summer travel plans, their strongest consideration is whether places are regularly cleaned. Additionally, consumers are highly concerned with restrictions in place at their destinations (e.g., stay-at-home orders, quarantine requirements, status of reopenings), suggesting that as states reopen, more “considerers” may begin to book summer travel.

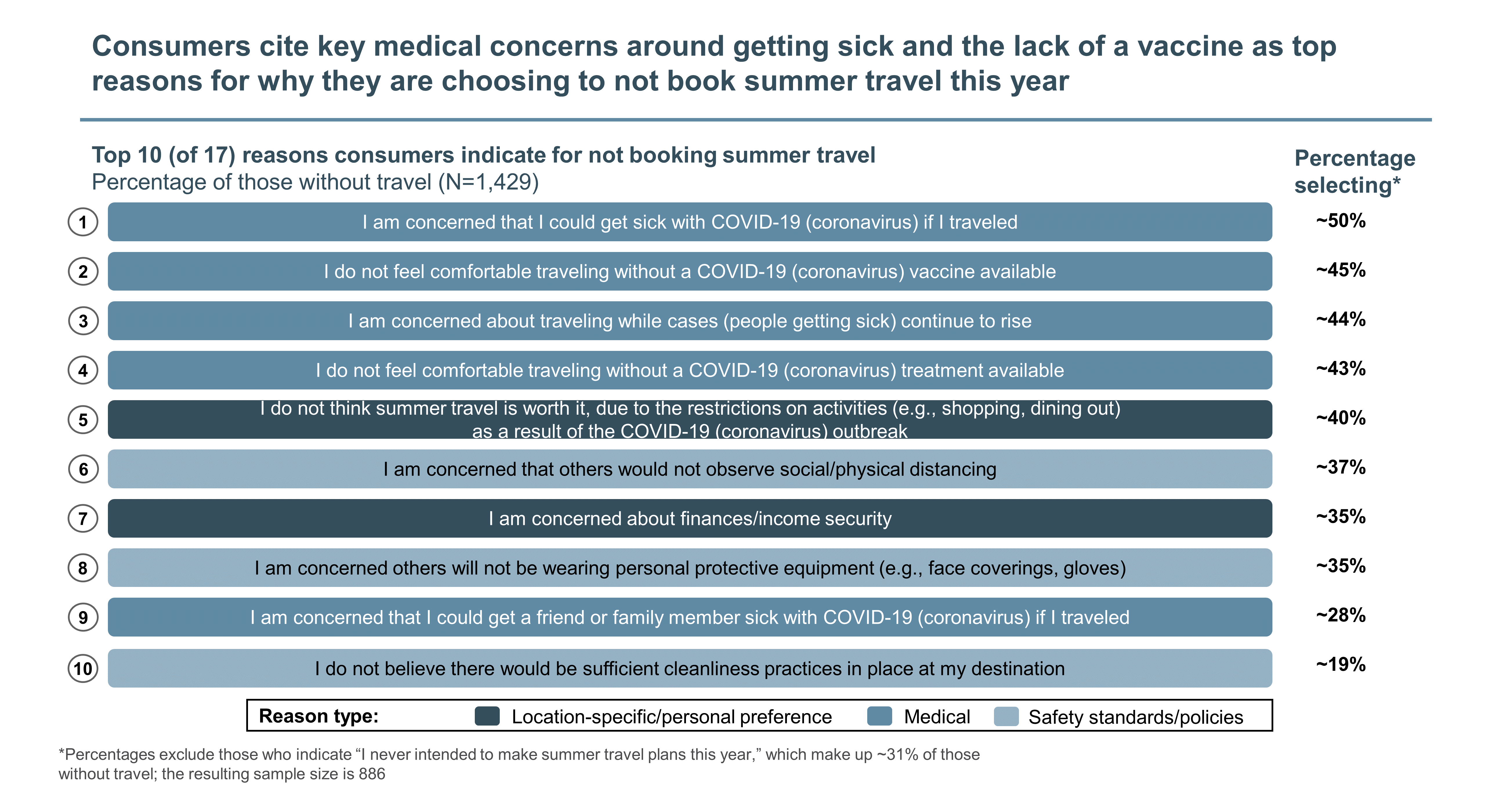

Of the nearly 60% of consumers who do not anticipate traveling this summer, ~31% never intended to make travel plans this year. When excluding this group from those without travel plans, the top reasons for not booking travel are concerns about getting sick with COVID-19 (~50%), an unwillingness to travel without a COVID-19 vaccine developed (~45%) and concerns about traveling as the number of COVID-19 cases continues to rise (~44%).

Interestingly, only ~35% of nontravelers listed income security as a reason for not traveling, suggesting financial position is less of a concern than COVID-19 health risks as it relates to summer travel plans.

We examined which measures consumers indicated they want to see before resuming traditional travel and retail/entertainment activities. The results suggest businesses have a significant role to play in helping shape the return of their customers.

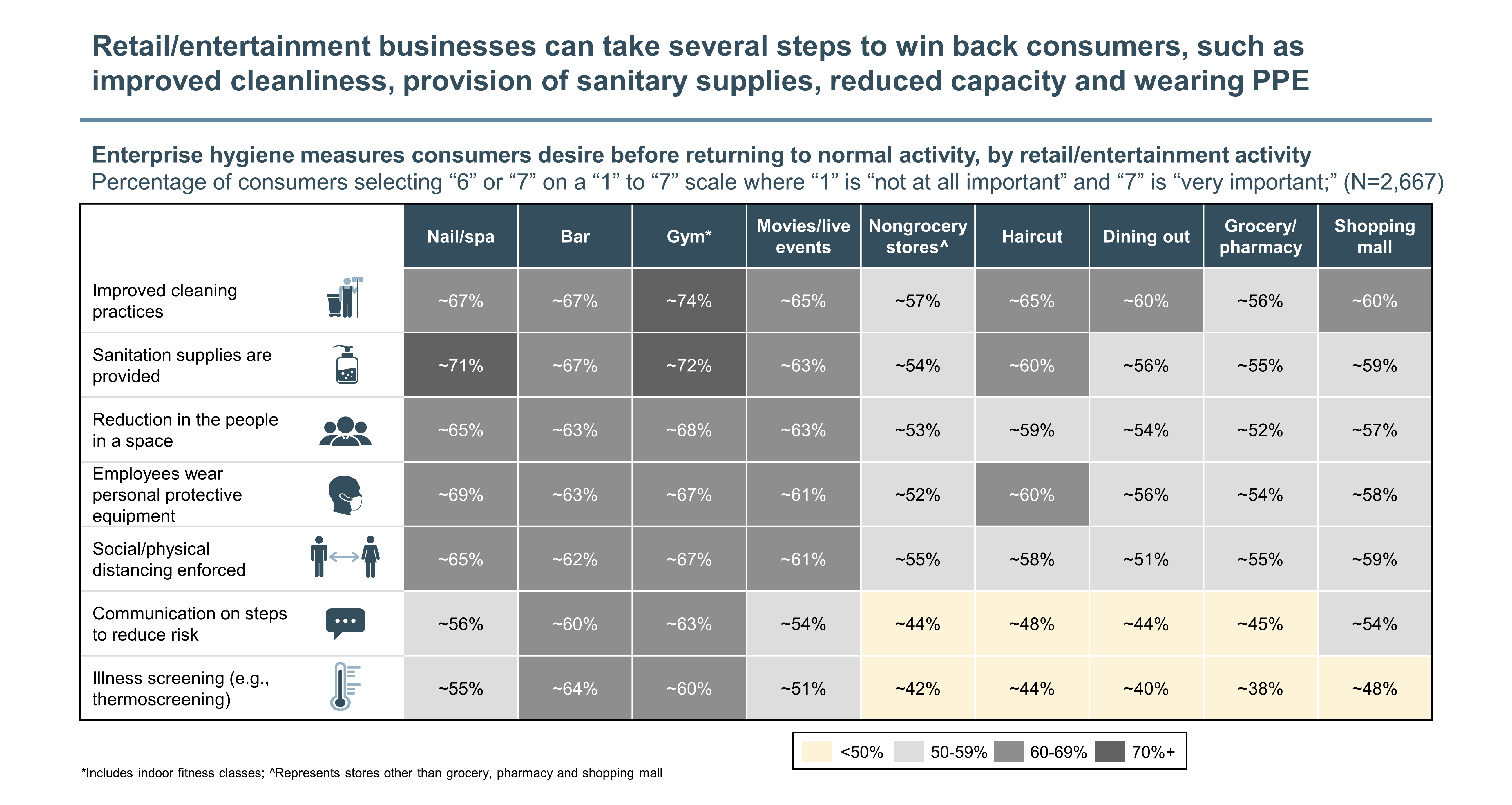

Within retail/entertainment activities, consumers indicated a number of enterprise hygiene measures were critical for resuming normal activity. Some of these measures are easier, lower-cost options, such as effectively communicating the steps being taken to reduce risk. However, others have clear cost implications, such as investing in improved cleaning practices or choosing to implement capacity constraints alongside social distancing.

Many of these measures may become table stakes for businesses seeking to reopen. Others may pose significant hurdles for businesses to implement; for example, capacity constraints in restaurants may make operations unprofitable.

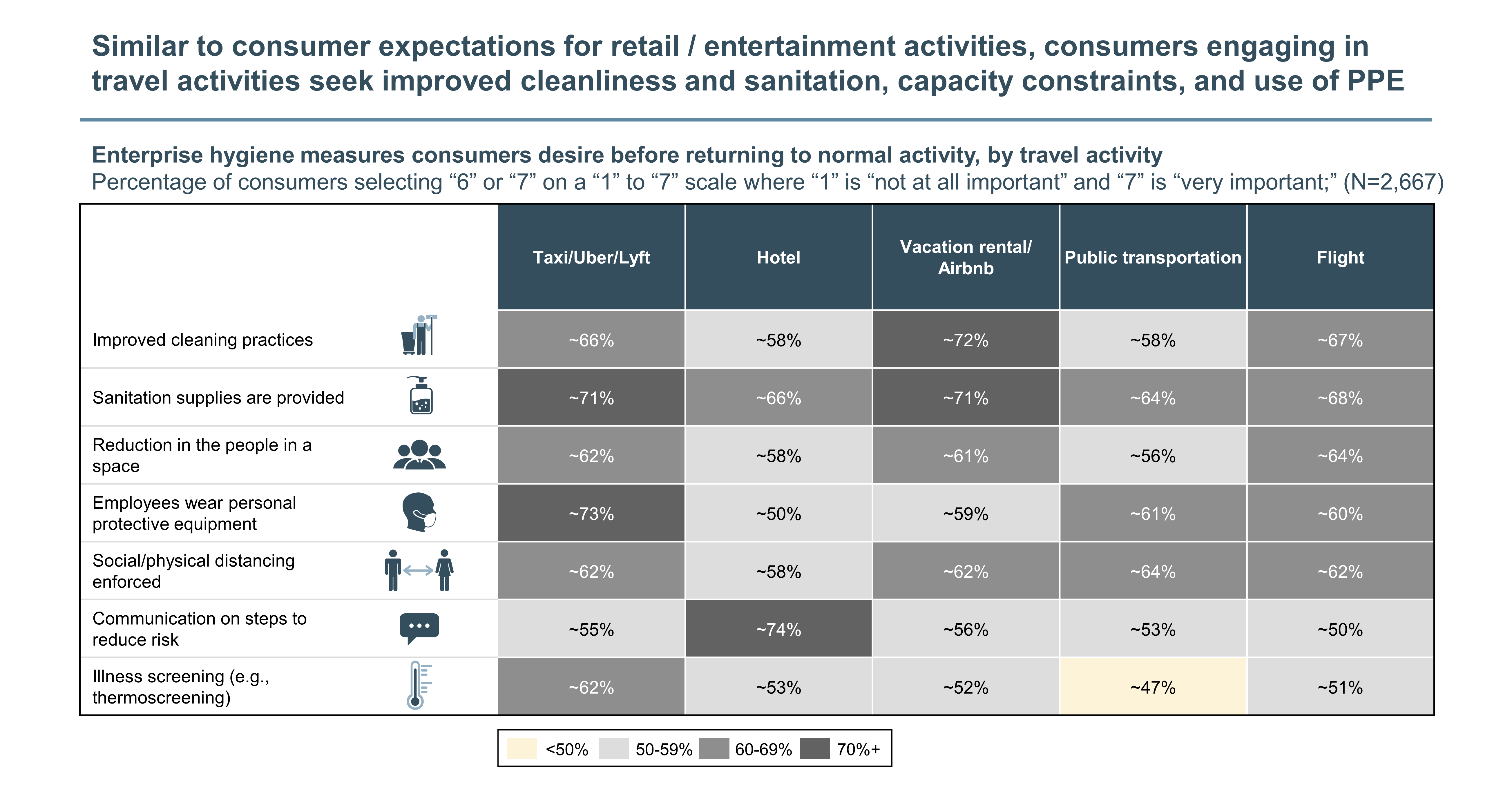

Within travel activities, a majority of consumers also find enterprise hygiene measures critically important to resuming normal activities.

The unique nature of guest turnover within the travel space creates additional issues around feasibility of implementing various measures, such as improved cleaning, offering sanitizers and capacity constraints. Hotel operators, airlines, rideshare companies and others must evaluate which measures can be implemented without constraining operations to the point of unprofitability.

As a reminder, we’ll be conducting recurring consumer pulse surveys approximately every two weeks to continually monitor consumer attitudes and behaviors.

We understand that many of our clients are facing new disruptions and increased uncertainty in their business outlook. In addition to this work, all of our sector teams are preparing insights on how the latest developments are shifting consumer attitudes, international business flows, commodities pricing and commercial priorities. Some of these changes are likely to endure well beyond when the current pandemic has passed. While many of these changes will create challenges, there will also be new opportunities that emerge. We will be sharing our ideas and insights through our website and other media over the coming days and weeks.

We wish good health to you and your loved ones, and we look forward to continuing to support our clients through this difficult time.

To continue the discussion, please don’t hesitate to contact us.