COVID-19 in the US: Consumer Insights for Businesses — Edition 3, Part 1

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

In partnership with Civis Analytics, we’re publishing a series of insights on the consumer response to COVID-19. Our goal is to help our consumer-facing clients monitor sentiment and behaviors as they take shape during this unprecedented period.

At the same time, we acknowledge that the pandemic is a humanitarian crisis first and foremost. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this crisis.

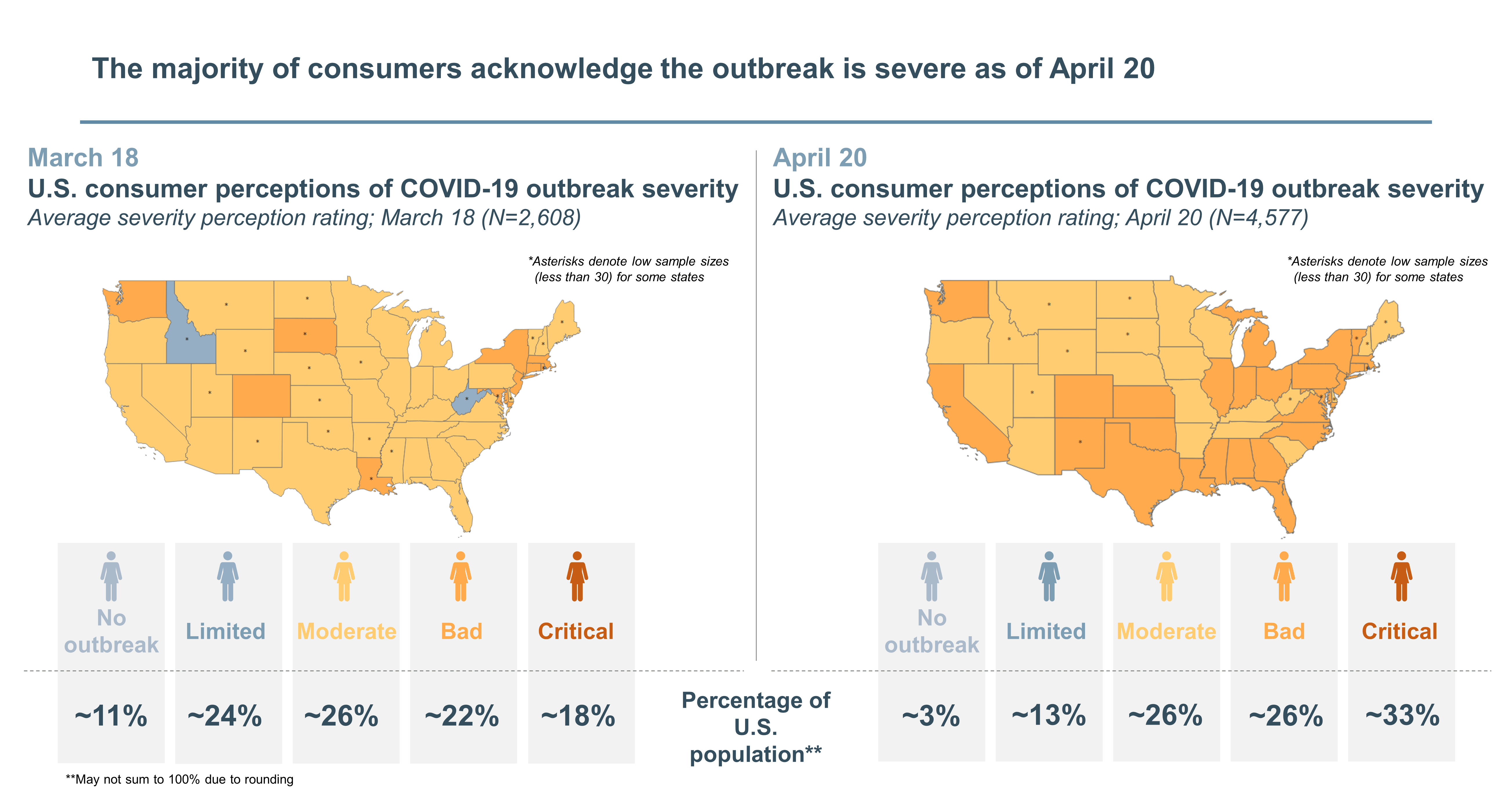

As of April 20, the majority of consumers acknowledge the outbreak is severe. Approximately 59% of consumers believe the severity of the outbreak in their area is either “bad” or “critical” (vs. ~40% on March 18). Only ~16% of consumers perceive “no outbreak” or “limited outbreak” in their area (compared to ~35% on March 18).

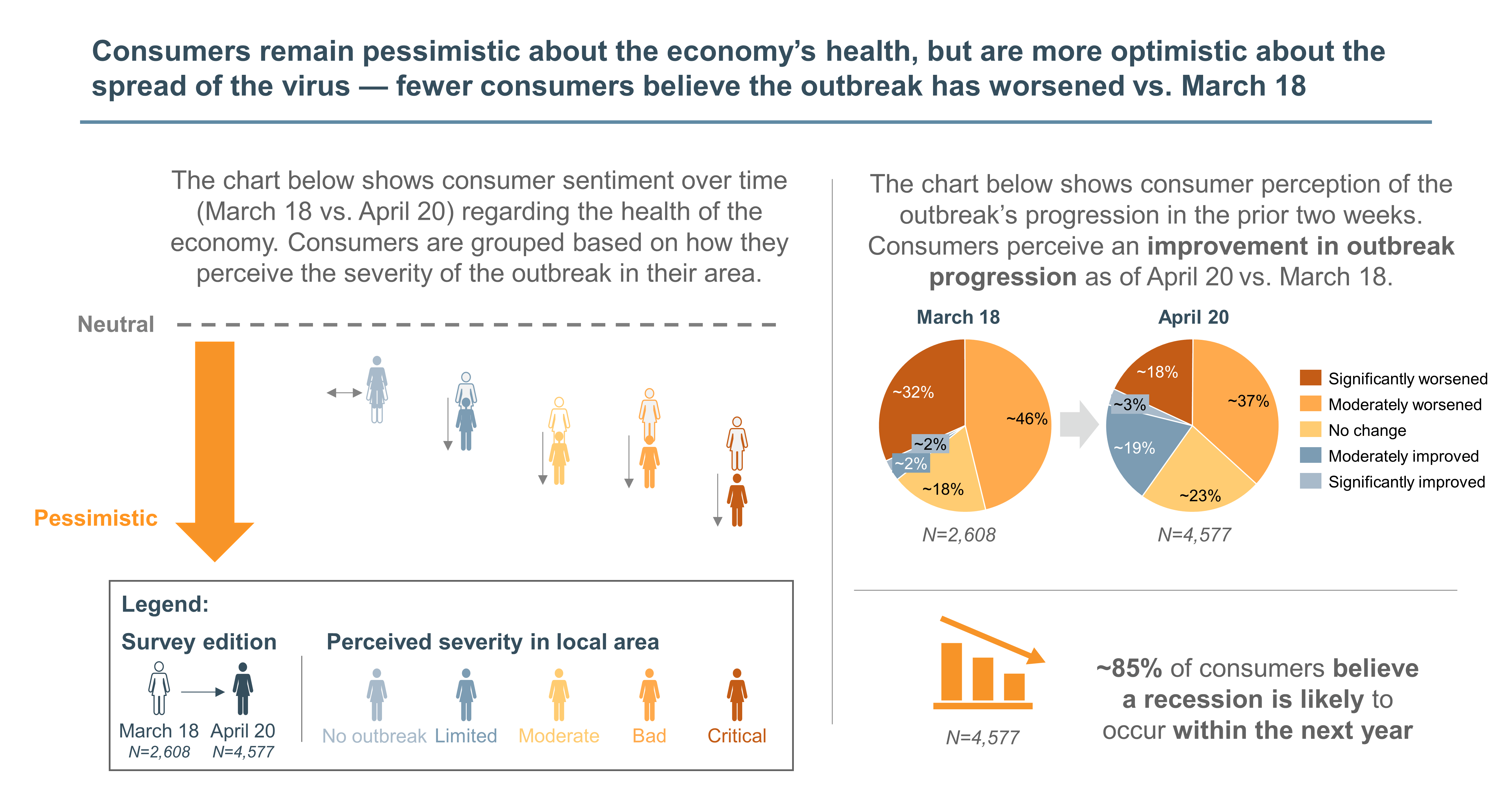

However, consumers are slightly more optimistic about the spread of the virus — responses suggest they believe it is slowing down. As of April 20, ~22% of consumers believe that the severity of the outbreak has either “significantly” or “moderately” improved (compared to just ~4% on March 18).

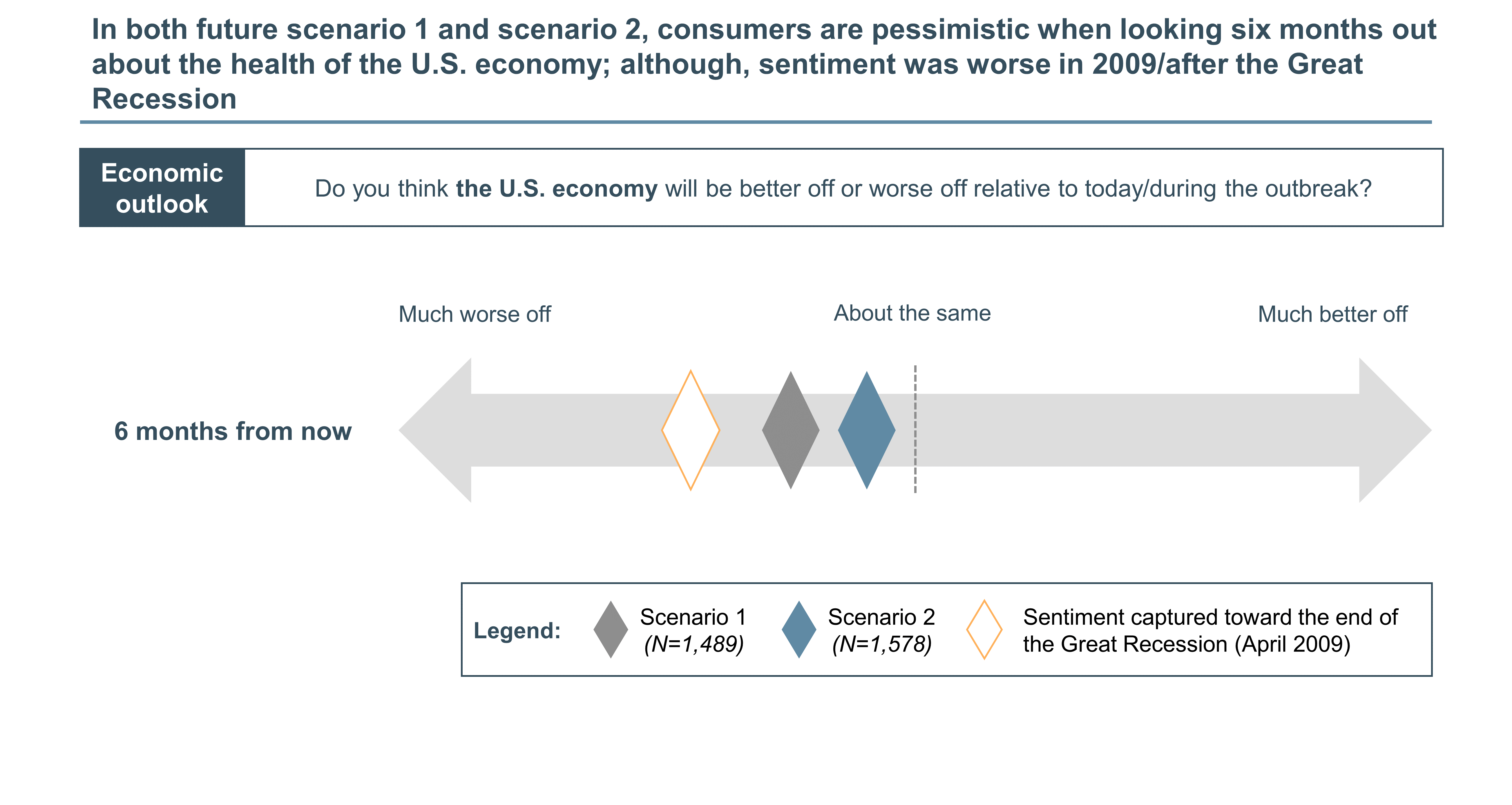

Consumers remain pessimistic about the economy overall. Approximately 85% of consumers believe a recession is likely to occur within the next year.

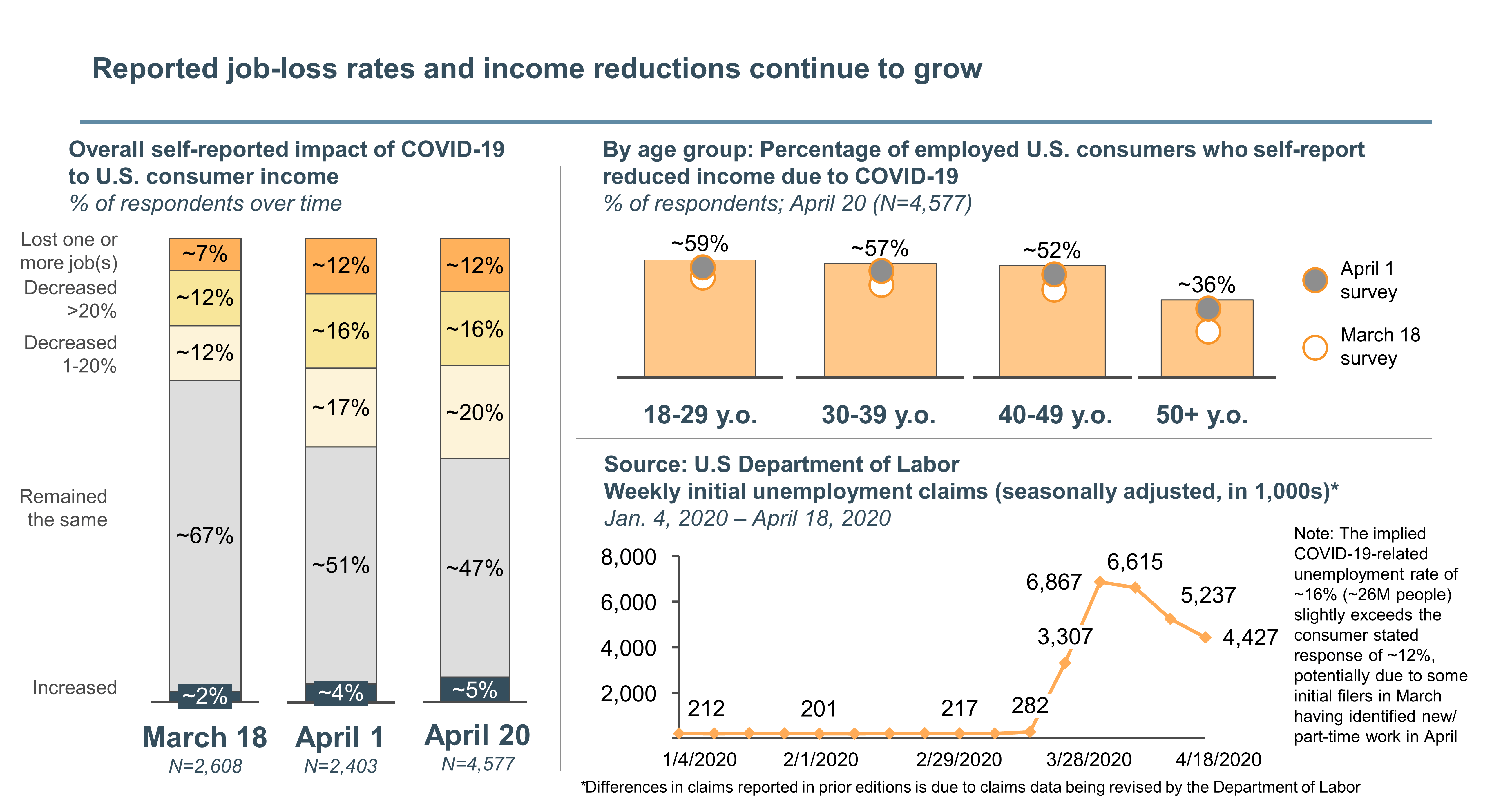

Consumers also report that job-loss rates and income reductions continue to grow. Approximately 48% of all consumers report a decline in their income vs. ~31% reporting so on March 18. Young respondents continue to be affected the most, with ~60% of respondents ages 18-29 reporting a decrease in income (compared to ~36% of respondents ages 50+). Consumers in our survey reported a job-loss rate of ~12%, which is slightly below government data that implies ~16% of consumers have lost their jobs since the outbreak began. The difference may potentially be driven by some initial filers in March having found new/part time work since filing.

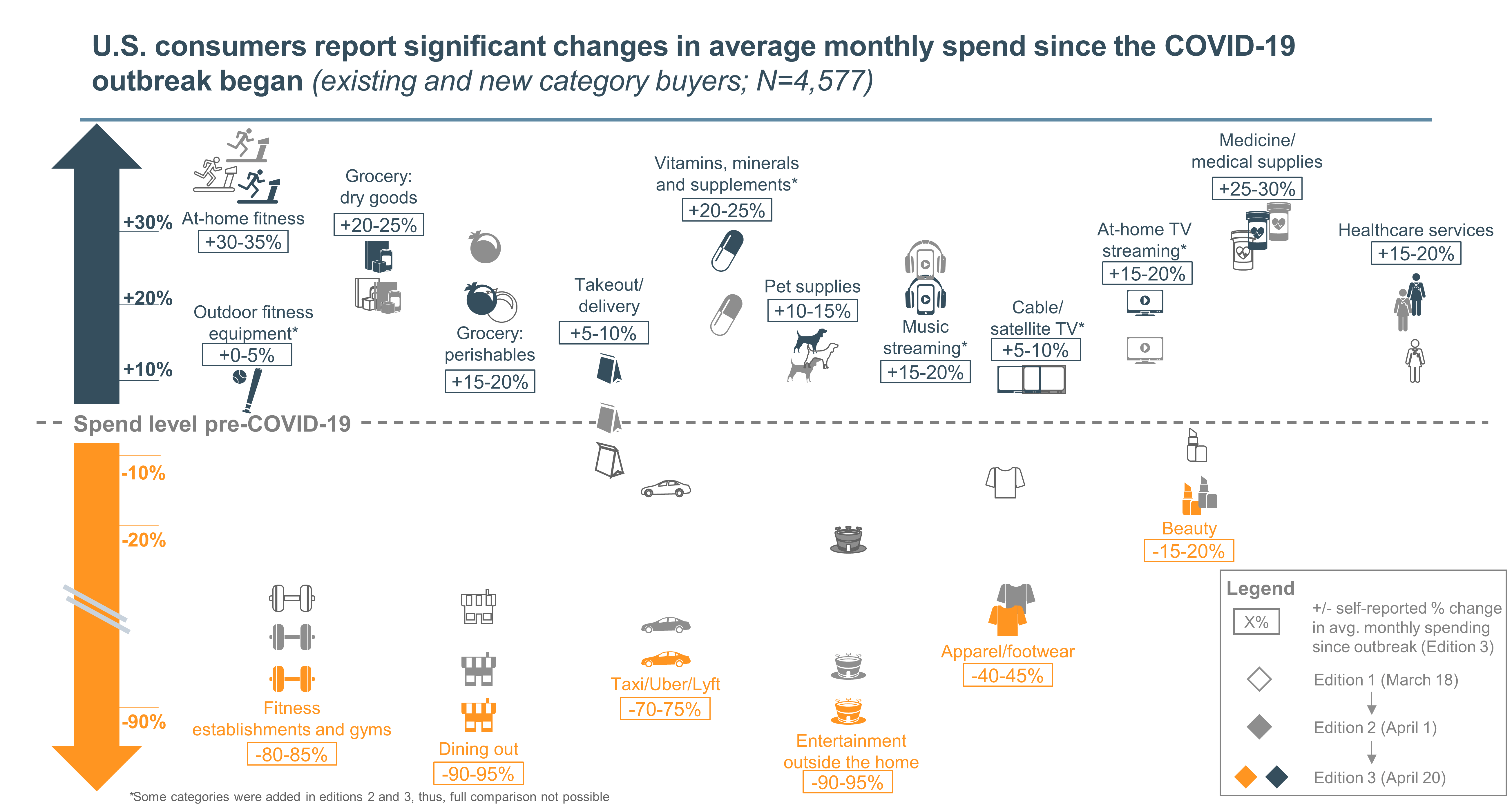

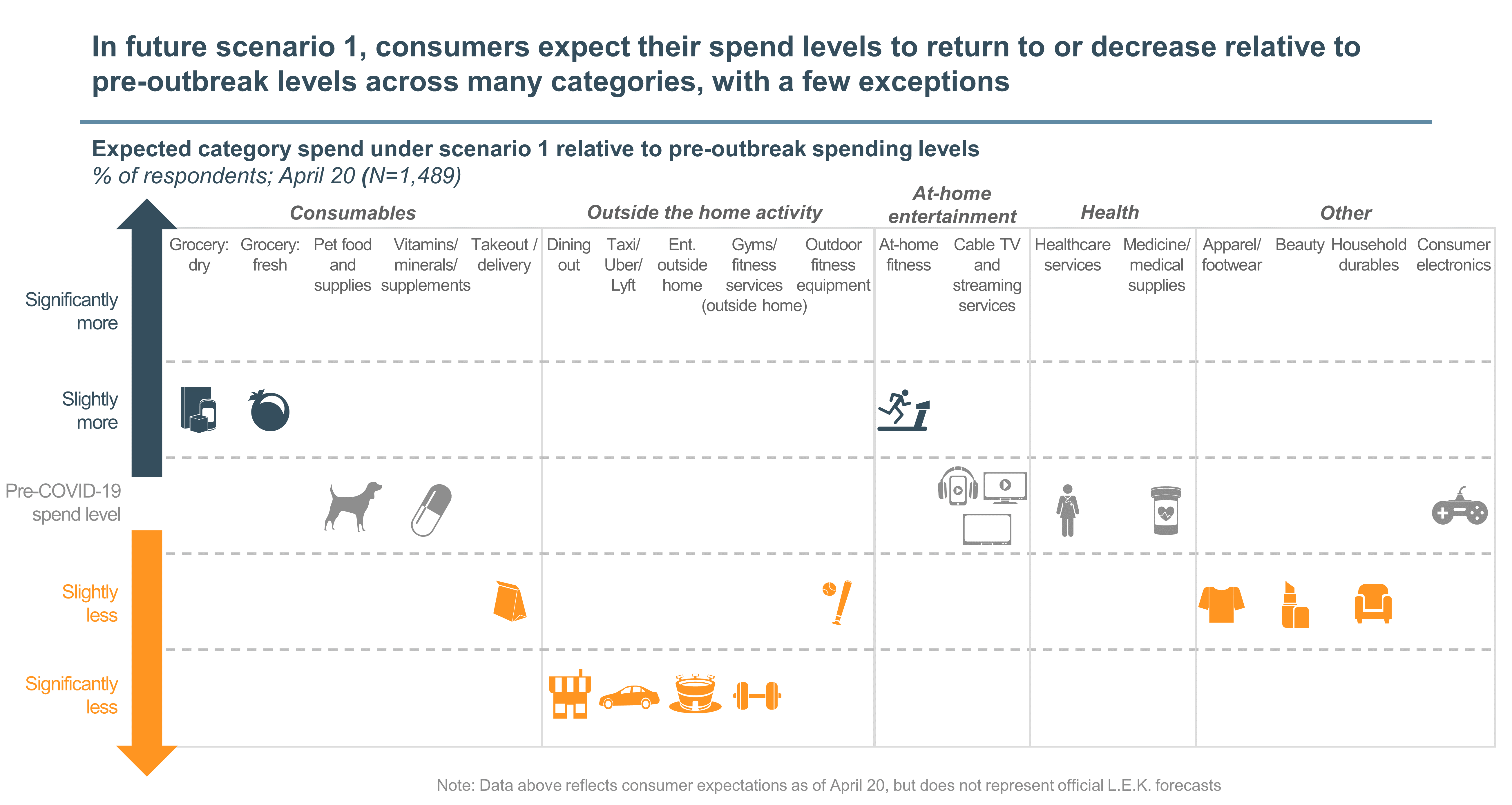

Consumer spend across a wide range of regular/monthly spending categories has changed significantly as a result of the outbreak.

Many regular/monthly spending categories have experienced a decline in average monthly spend levels, according to consumers, specifically:

Notably, takeout/delivery spend was down 10%-15% as of March 18 and roughly back in line with pre-outbreak spend levels according to our April 1 survey; in our latest edition, takeout spending is up 5%-10%. This feedback would suggest consumers are increasingly turning to takeout as an alternative to home cooking.

Consumers report increased average monthly spend for other categories since the beginning of the outbreak, specifically:

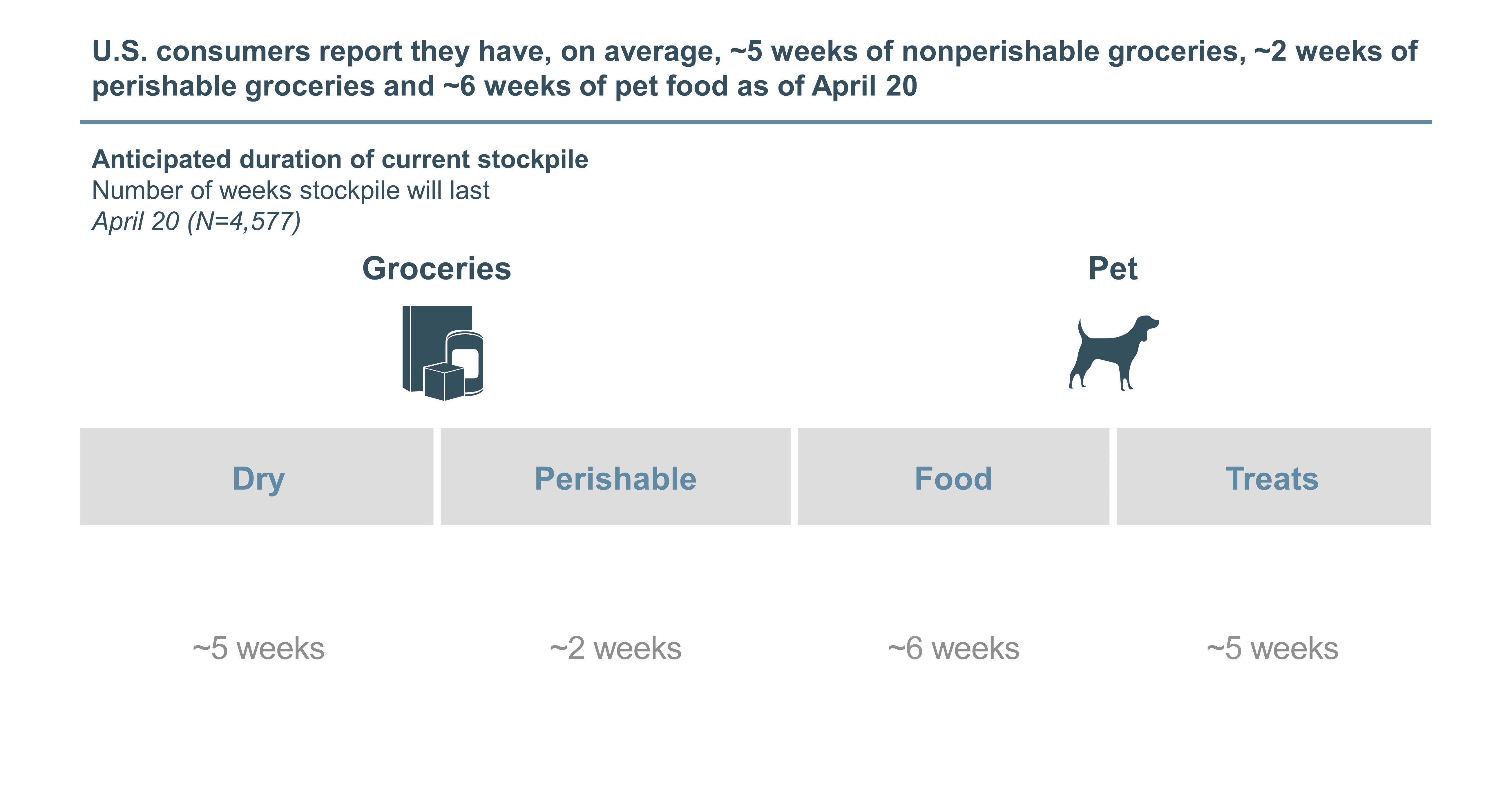

We also assessed the degree of stockpiling in this latest edition of the survey. We found that consumers report they have ~5 weeks of nonperishable groceries, ~2 weeks of perishable groceries and ~6 weeks of pet food as of April 20.

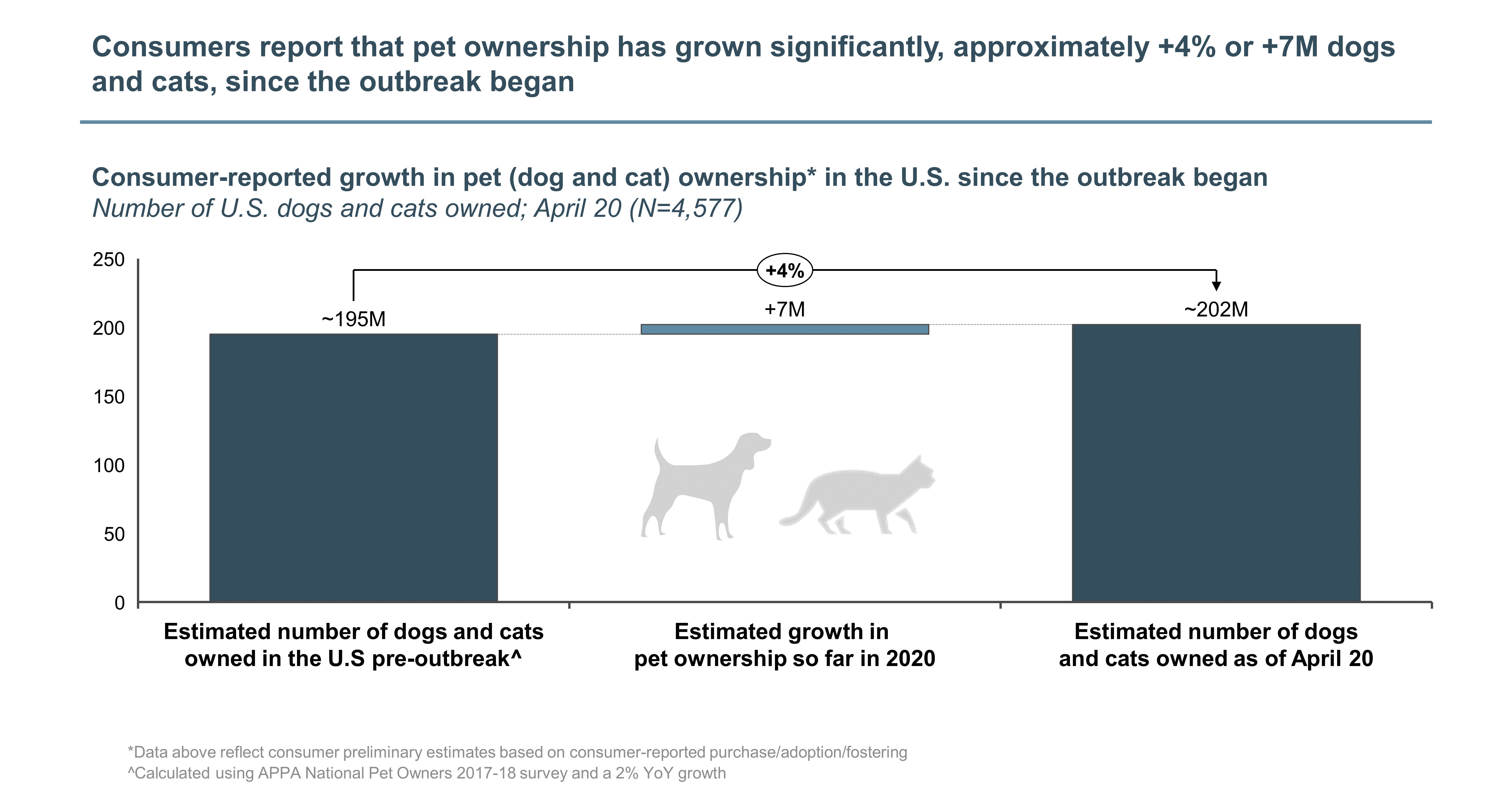

Additionally, we quantified the degree to which pet ownership has increased since the outbreak began. Consumer responses suggest that dog and cat ownership in the U.S. has increased ~4% or by ~7M-8M dogs and cats.

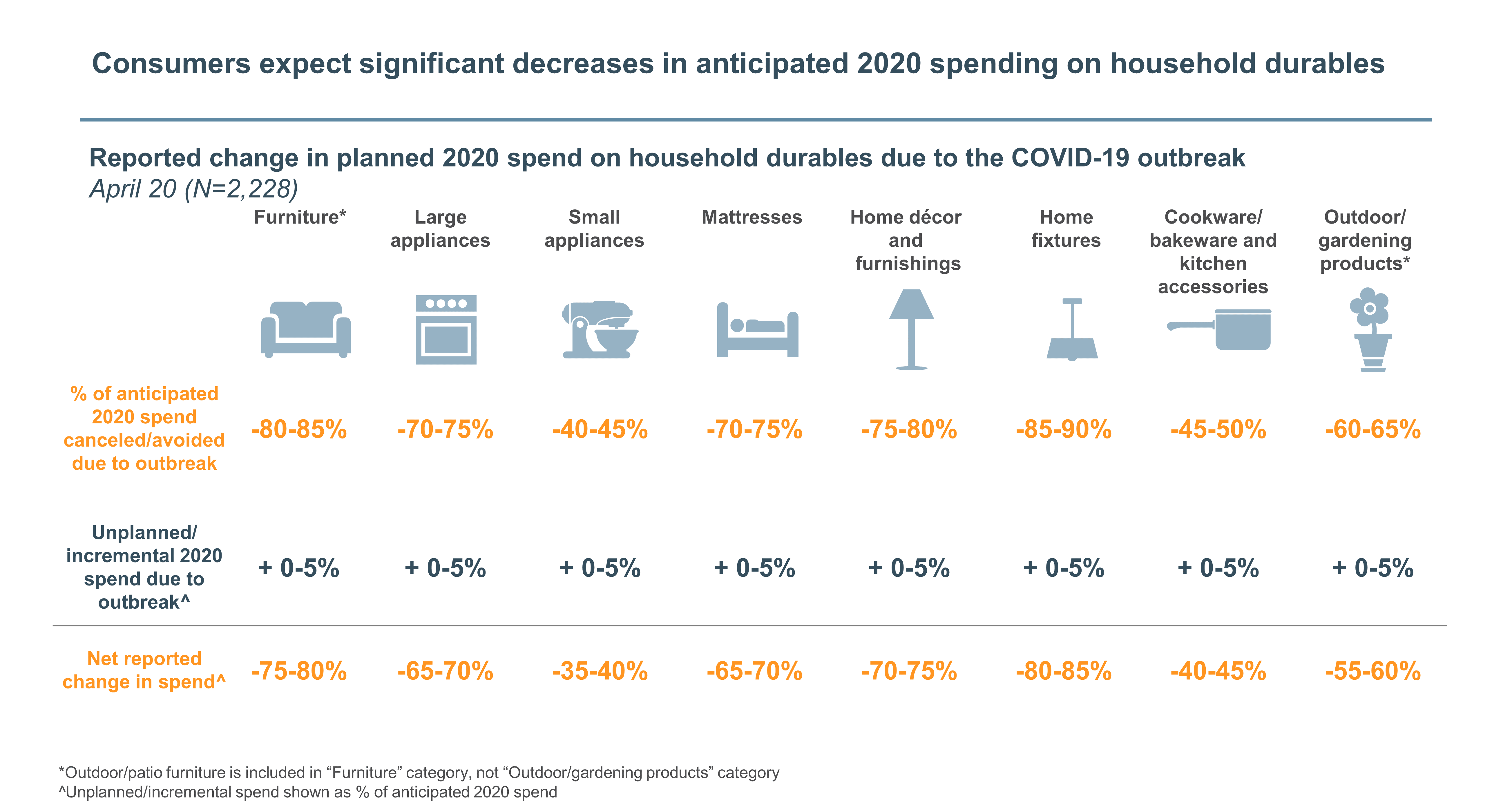

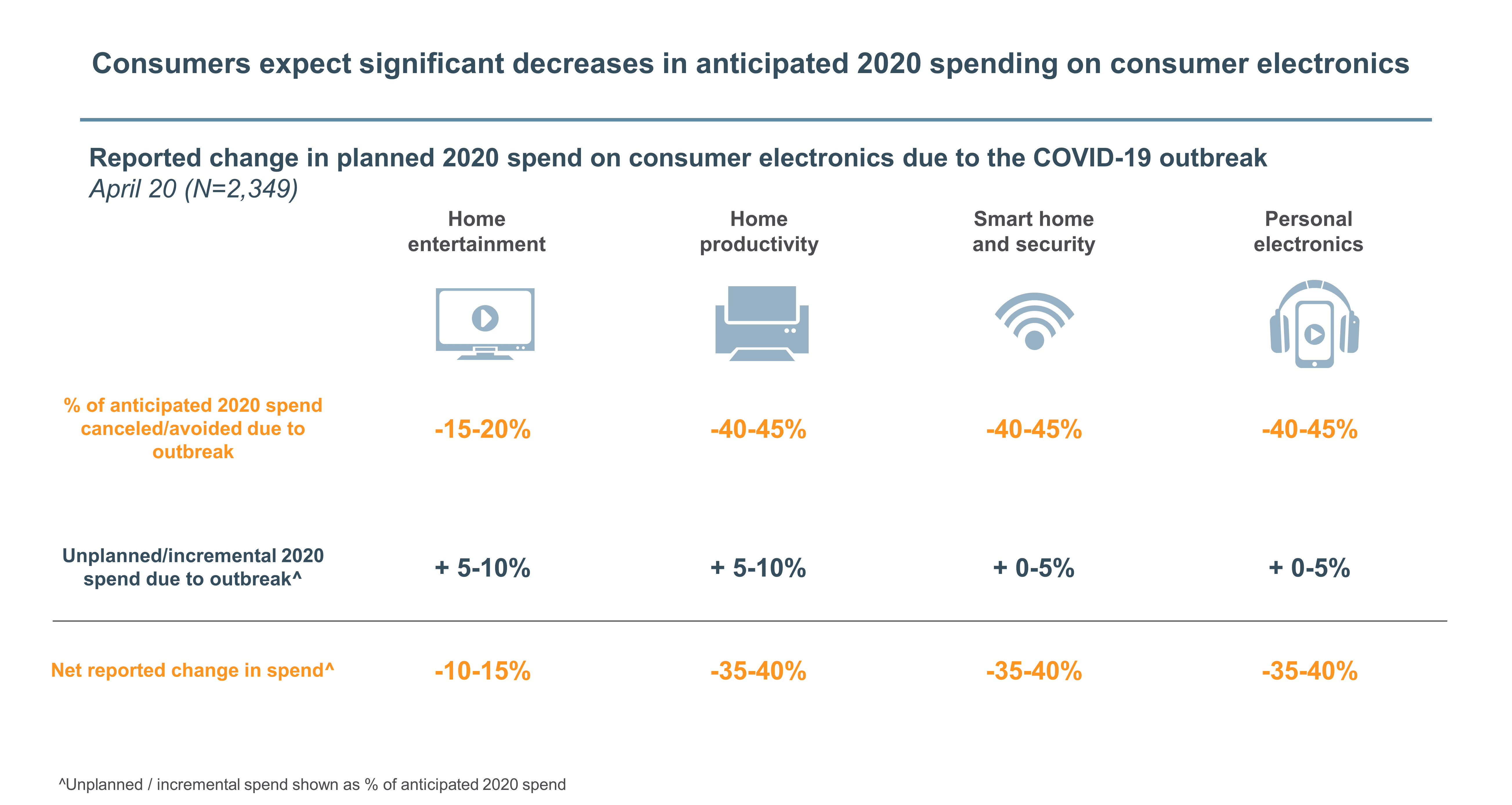

Consumers report that they plan to cancel or avoid a significant portion of anticipated spend during 2020 on household durable and consumer electronics subcategories (including any spend that has already been canceled or avoided). There appear to be higher rates of unplanned spend within home entertainment and home productivity. However, these categories are still net negative, as the unplanned spend is likely on lower-value items to support working from home, such as monitors and headphones.

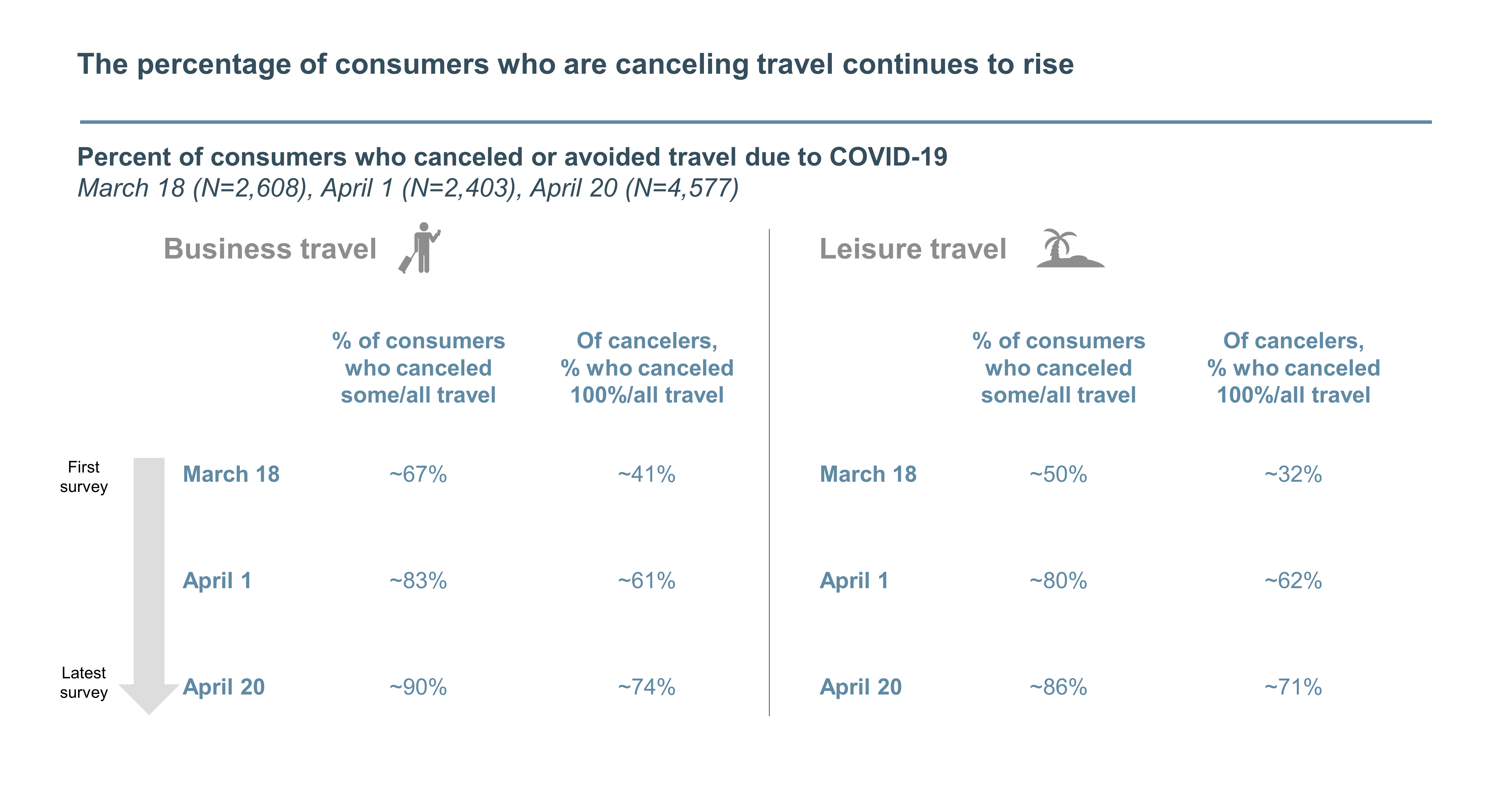

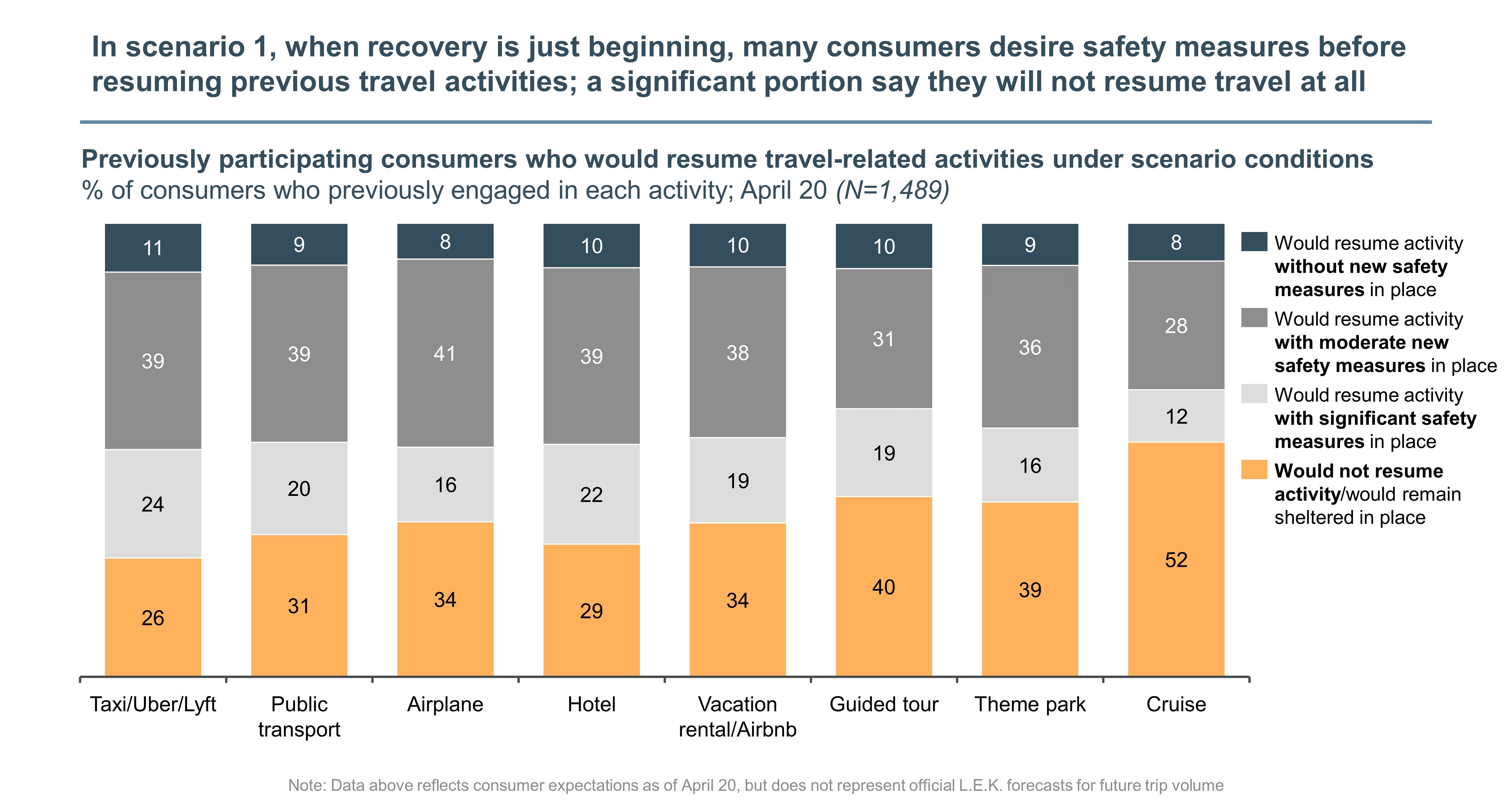

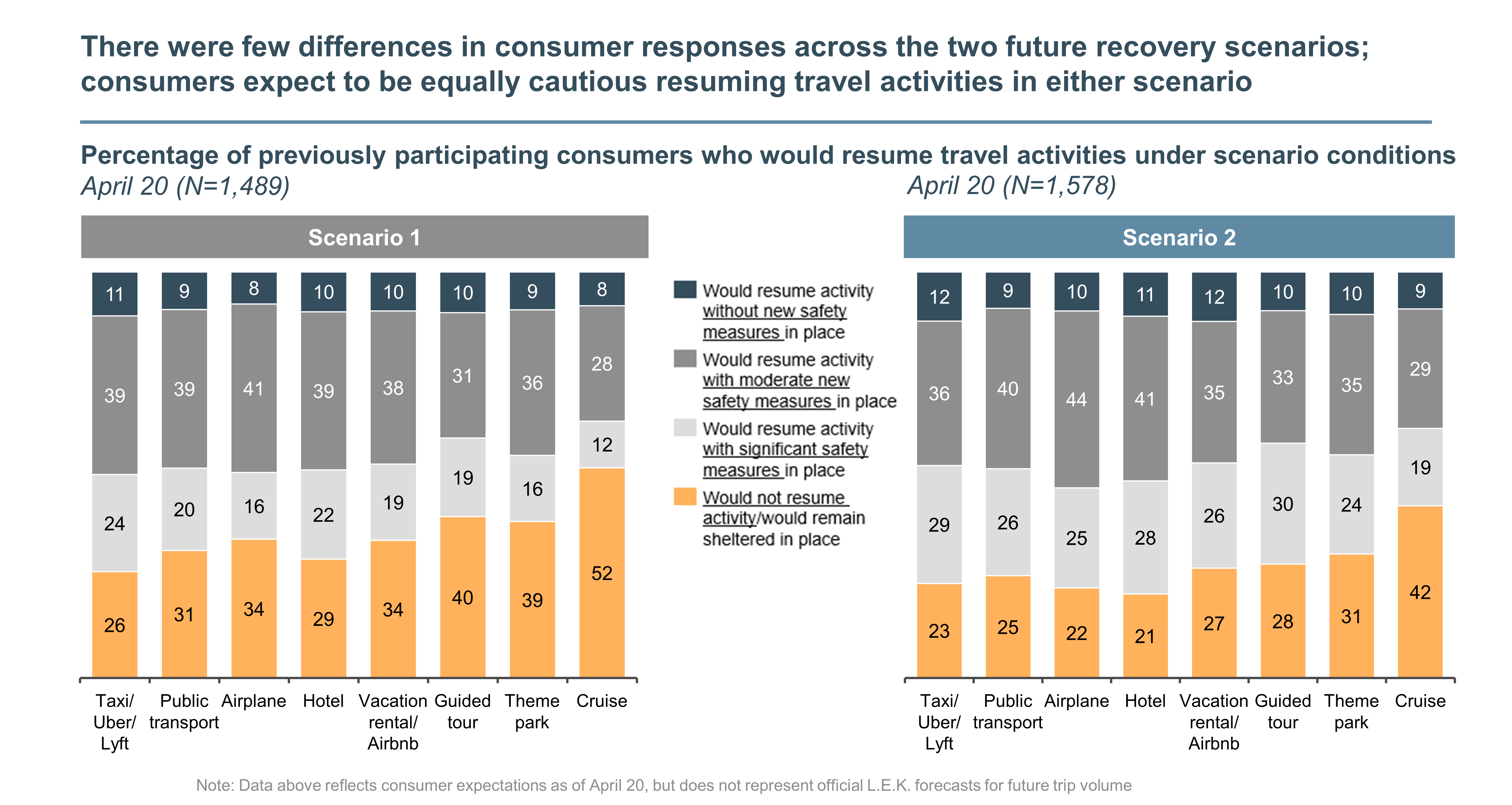

As the outbreak progresses, the percentage of consumers canceling travel continues to rise. Approximately 90% of business travelers and ~86% of leisure travelers canceled at least some of their travel plans, up from ~83% and ~80%, respectively, on April 1.

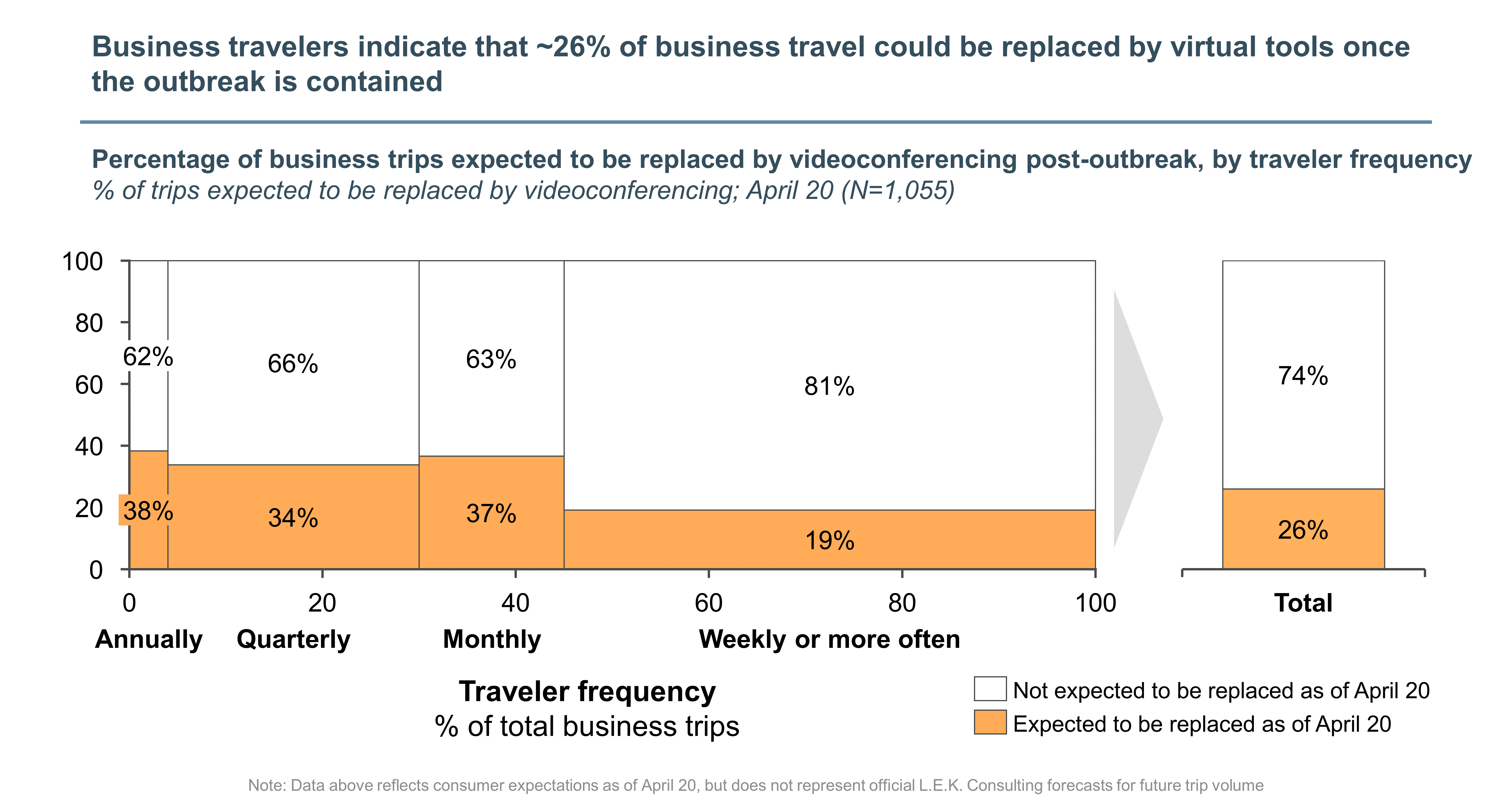

Business travelers indicate a strong willingness to replace large portions of business travel with virtual tools (e.g., videoconferencing). While frequent travelers anticipate lower rates of replacement, the overall amount of travel estimated to be replaced, based on consumers’ responses, is ~26%.

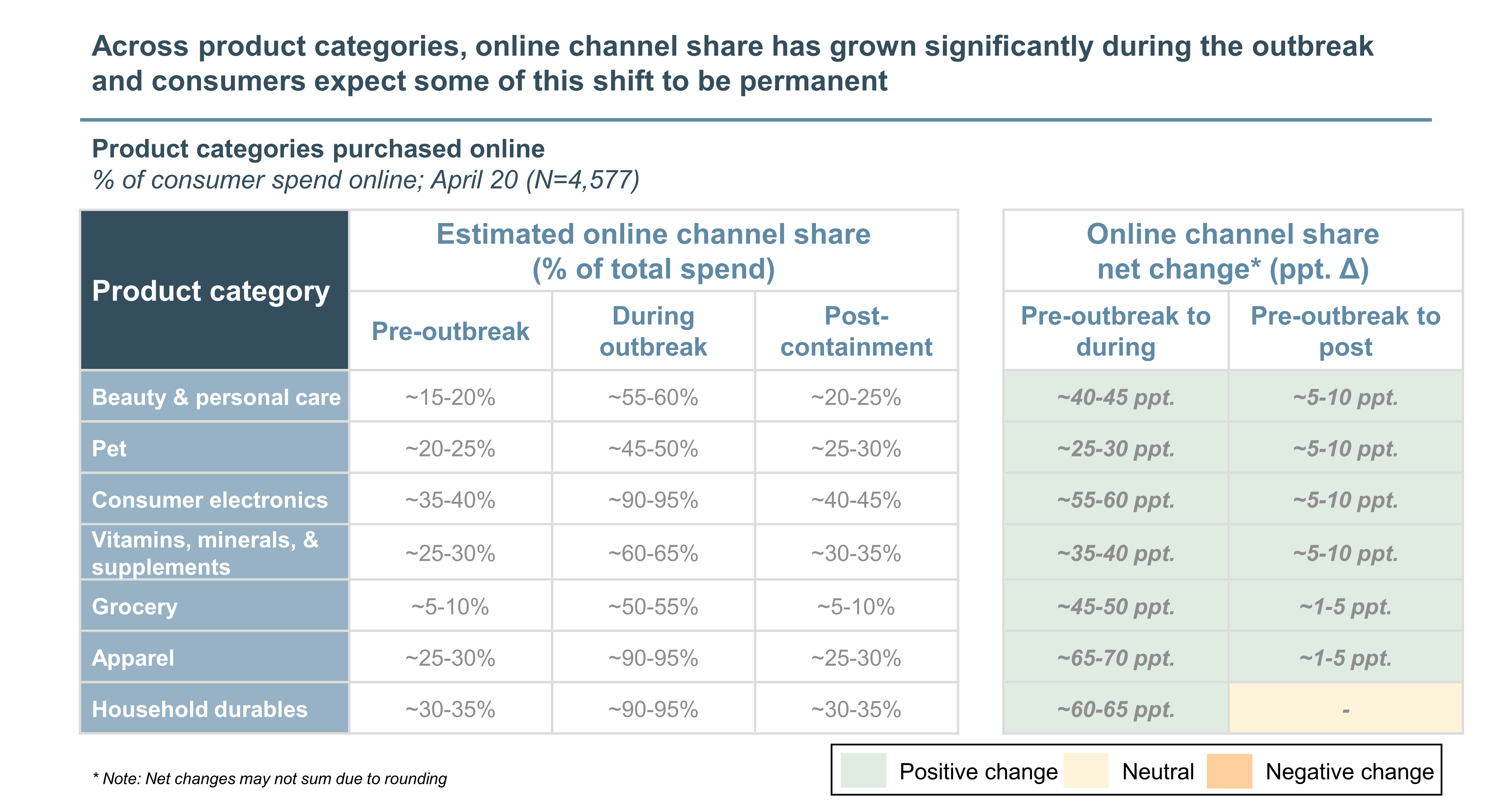

Consumers report a significant increase in the portion of spend made online across product categories, fueled by the closures of brick-and-mortar retail and service locations.

Categories for which retailers are not deemed “essential” have seen the largest shifts online, such as apparel, household durables and consumer electronics.

Once the outbreak is contained, consumers expect some of the shift online to be permanent.

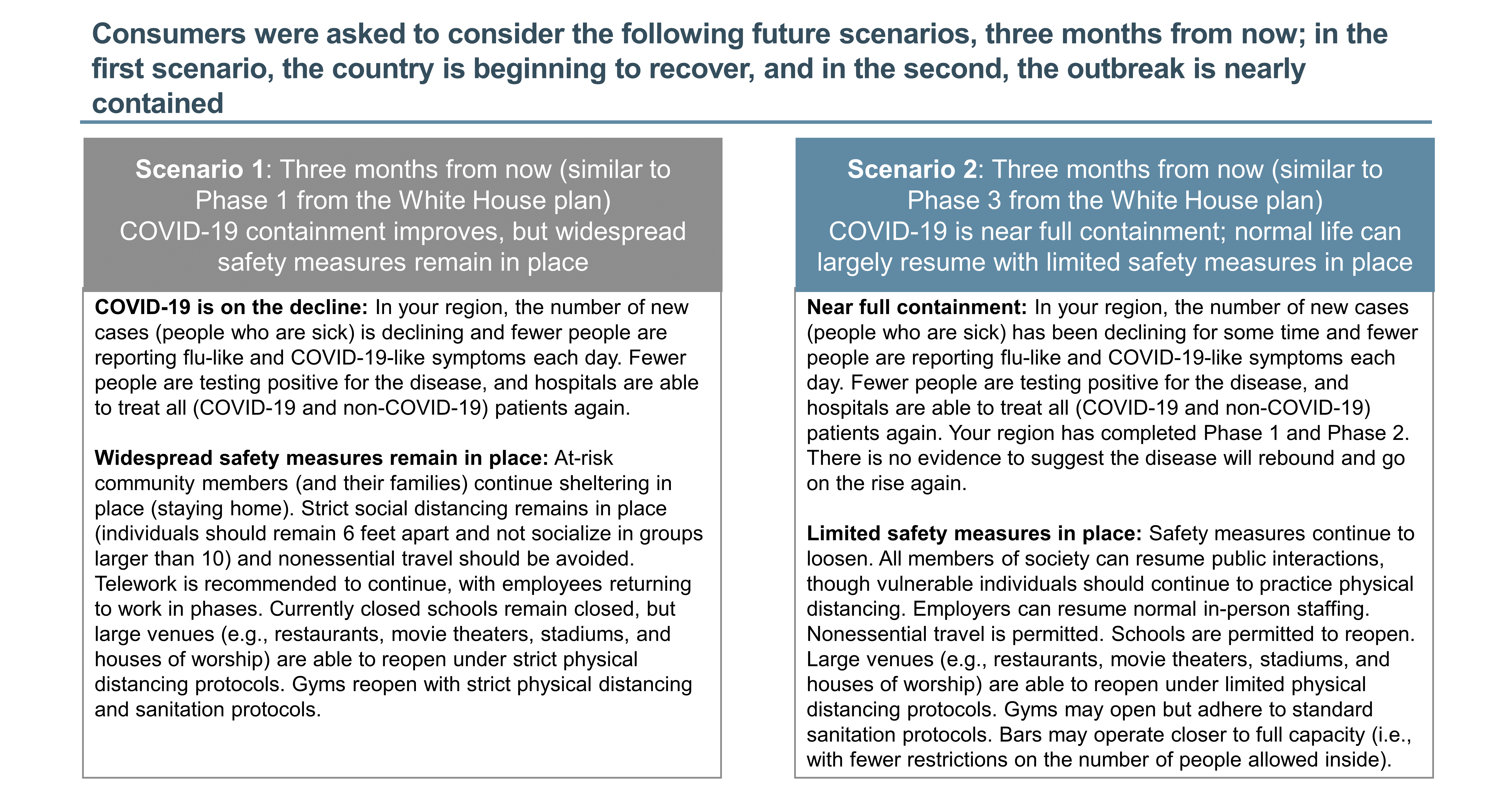

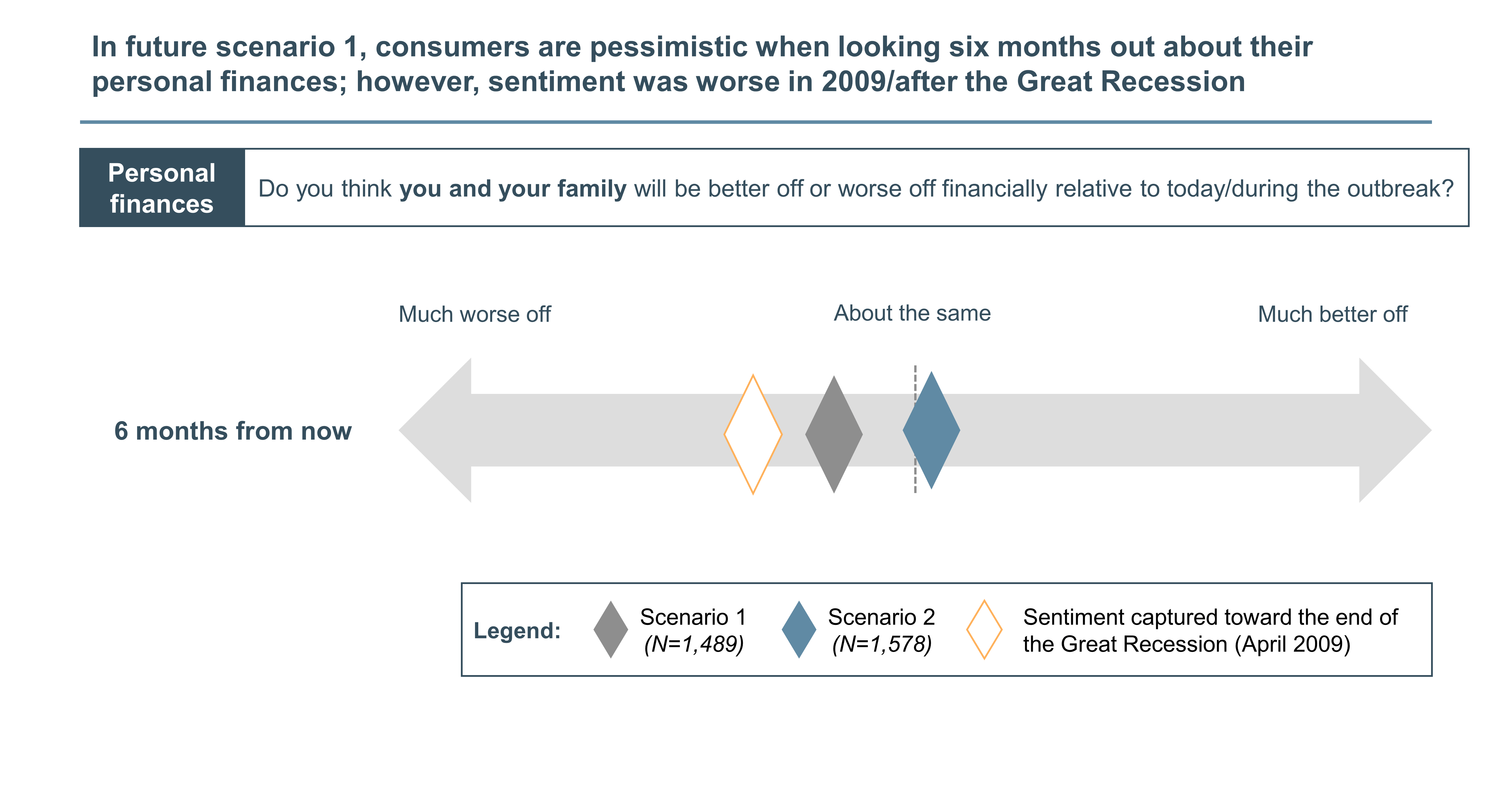

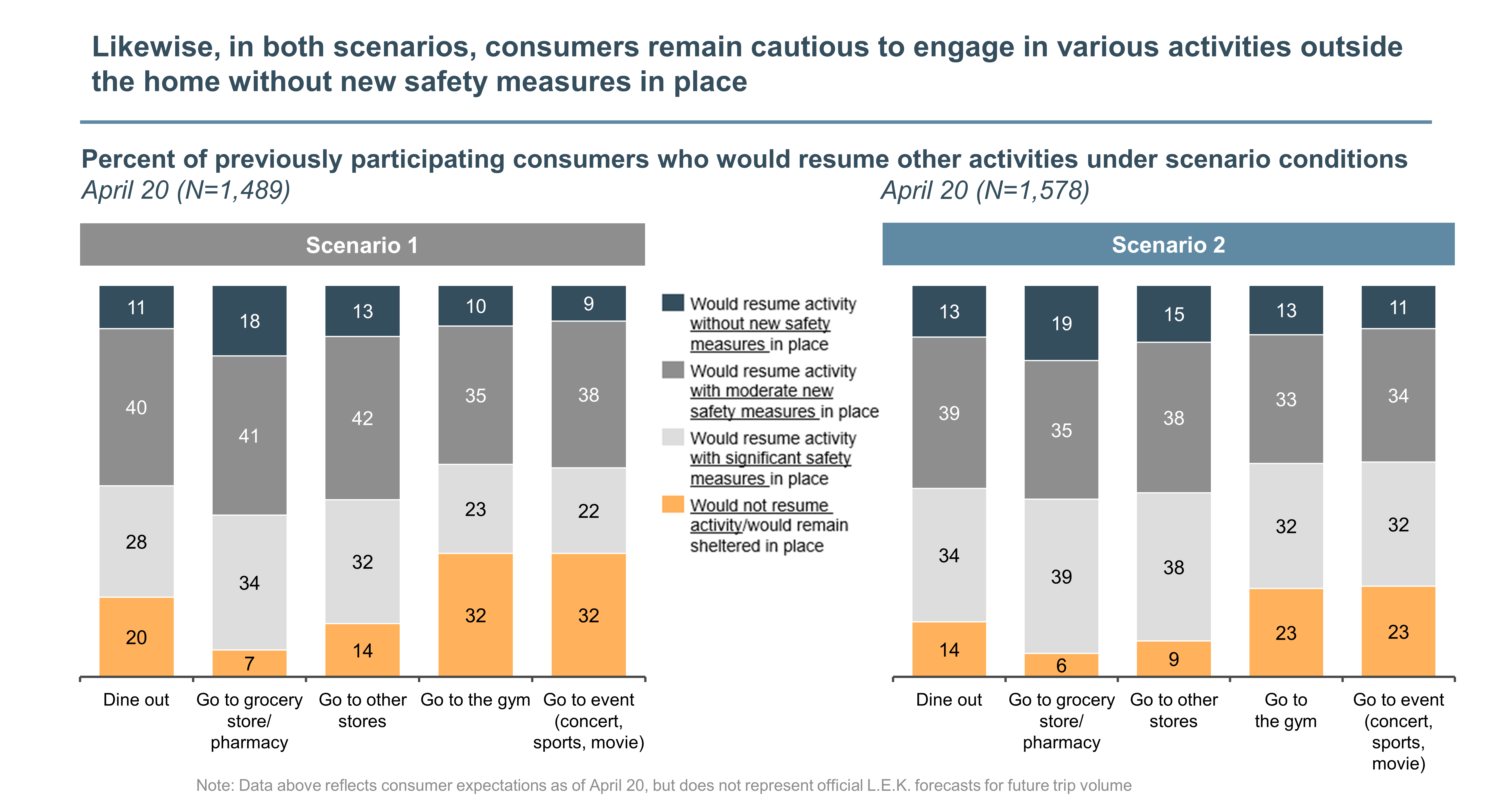

Consumers were asked to consider two different future recovery scenarios: scenario 1 in which the country is beginning to recover and scenario 2 in which the outbreak is nearly contained in the country. Here’s what we found:

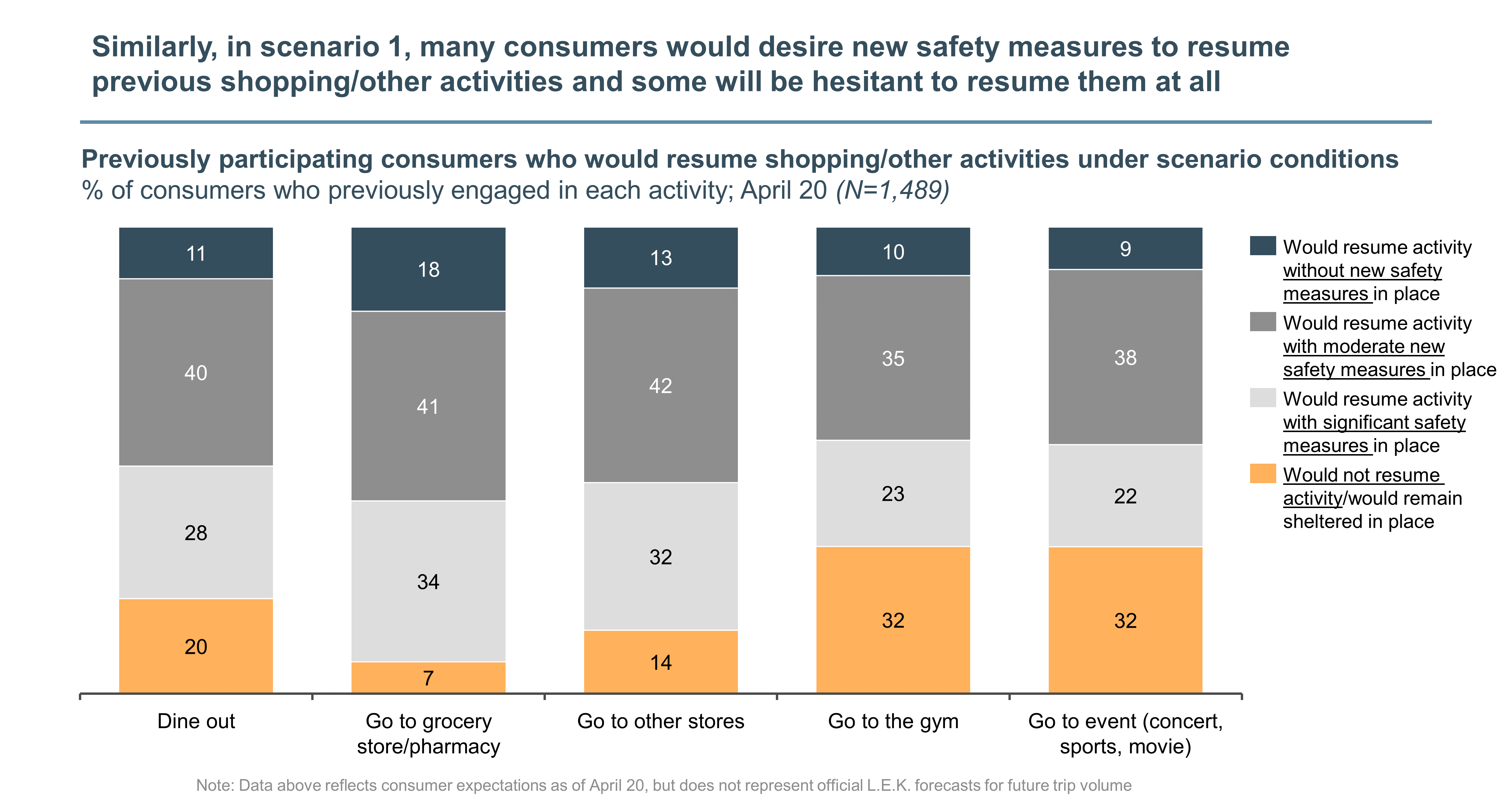

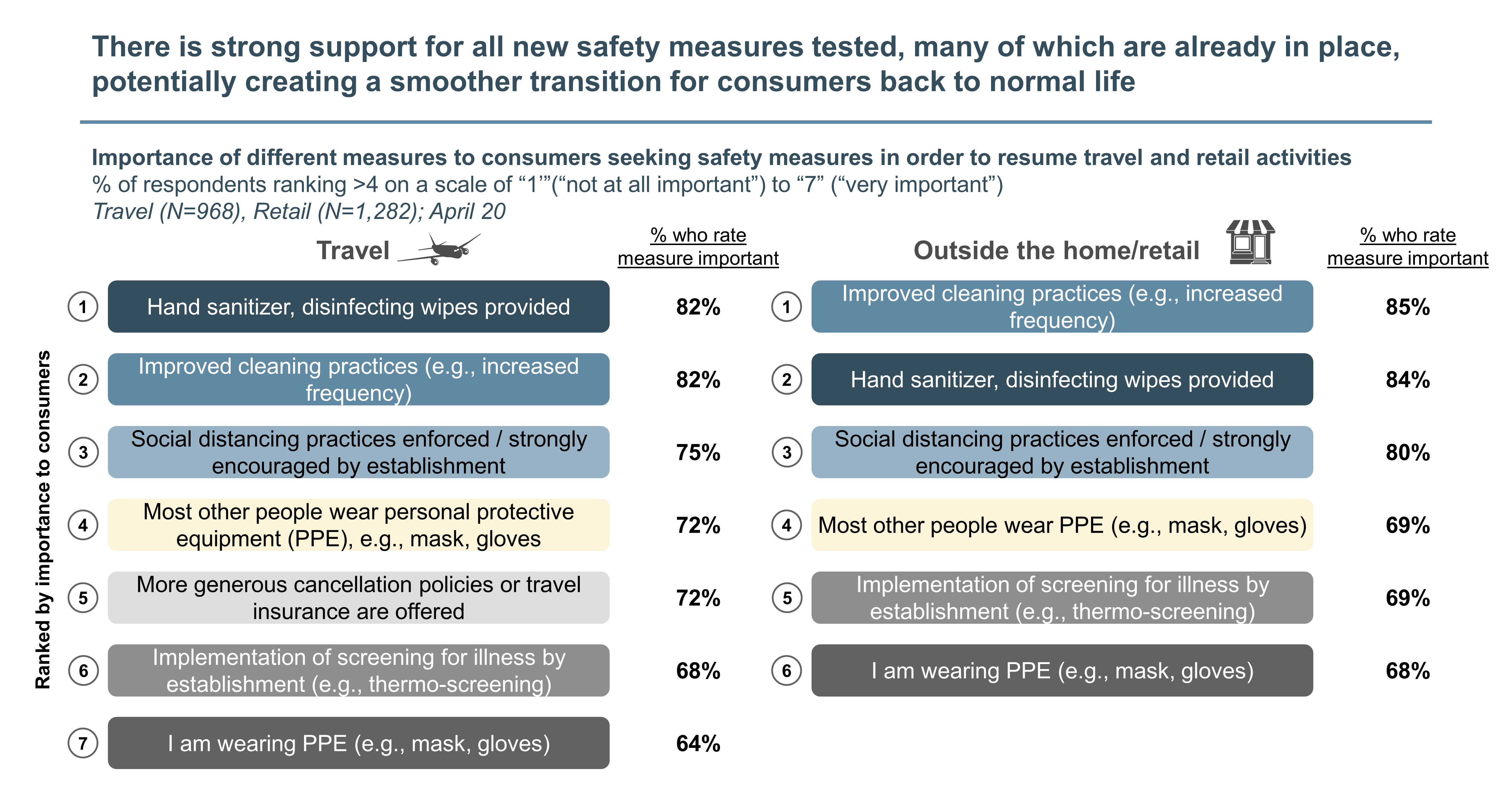

However, ongoing implementation of these measures could impact revenue and/or margins, whether it be due to greater investment in cleaning/sanitation supplies or the inability to host as many consumers within a store and/or an establishment at a given time.

As a reminder, we’ll be conducting recurring consumer pulse surveys approximately every two weeks to continually monitor consumer attitudes and behaviors.

We understand that many of our clients are facing new disruptions and increased uncertainty in their business outlook. In addition to this work, all of our sector teams are preparing insights on how the latest developments are shifting consumer attitudes, international business flows, commodities pricing and commercial priorities. Some of these changes are likely to endure well beyond when the current pandemic has passed. While many of these changes will create challenges, there will also be new opportunities that emerge. We will be sharing our ideas and insights through our website and other media over the coming days and weeks.

We wish good health to you and your loved ones, and we look forward to continuing to support our clients through this difficult time.

To continue the discussion, please don’t hesitate to contact us.