Summary

Over the past 18 months, the U.K. supermarket price war between the “big four” and continental hard discounters has intensified. It’s good news for consumers – since mid-2014 food and non-alcohol prices have declined at 2.1% per annum. But the question still remains, have the U.K.’s big four done enough to win the battle?

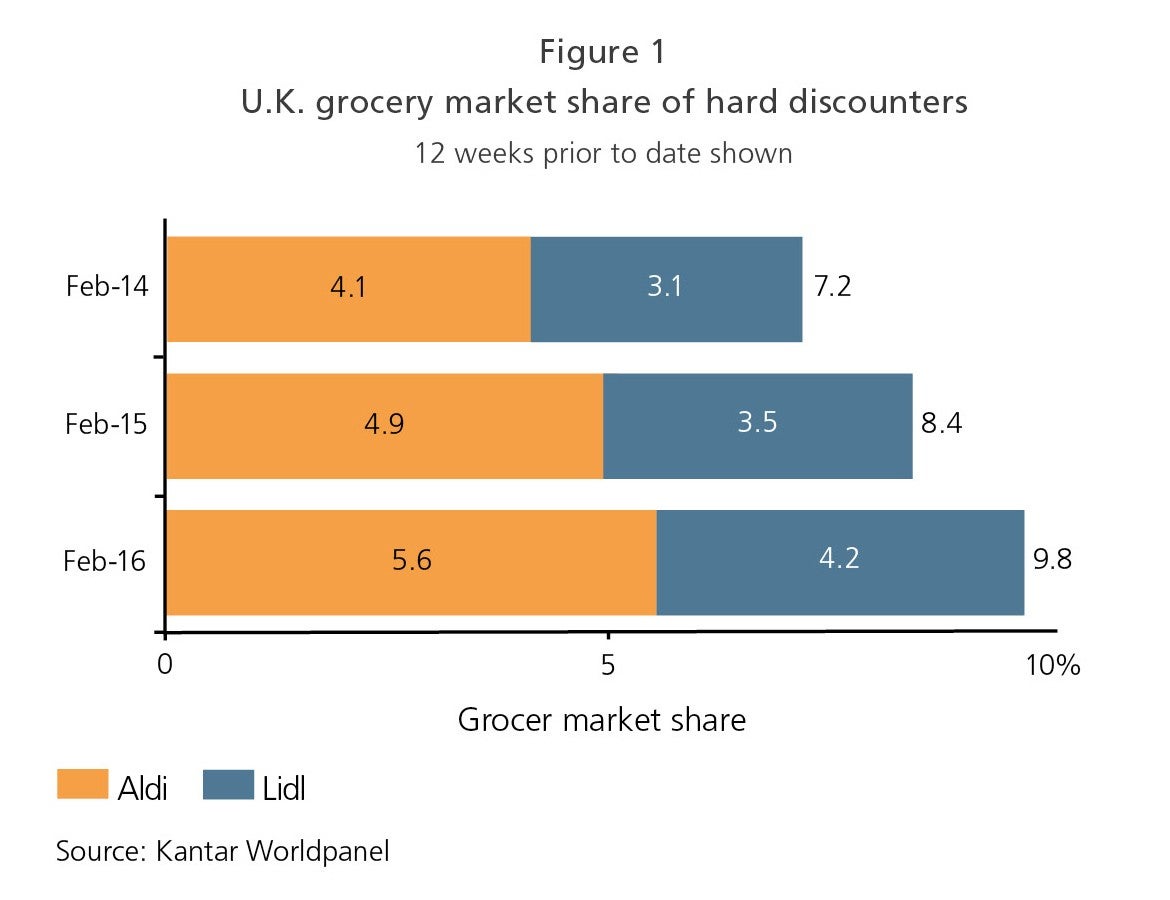

The answer, as L.E.K.’s Jonathan Simmons, Geoff Parkin and Jonathon Green argue in this Executive Insights – is not yet. Aldi and Lidl continue to steadily take U.K. grocery market share despite substantial efforts from the big supermarkets to close the gap on both national brands and private label goods.

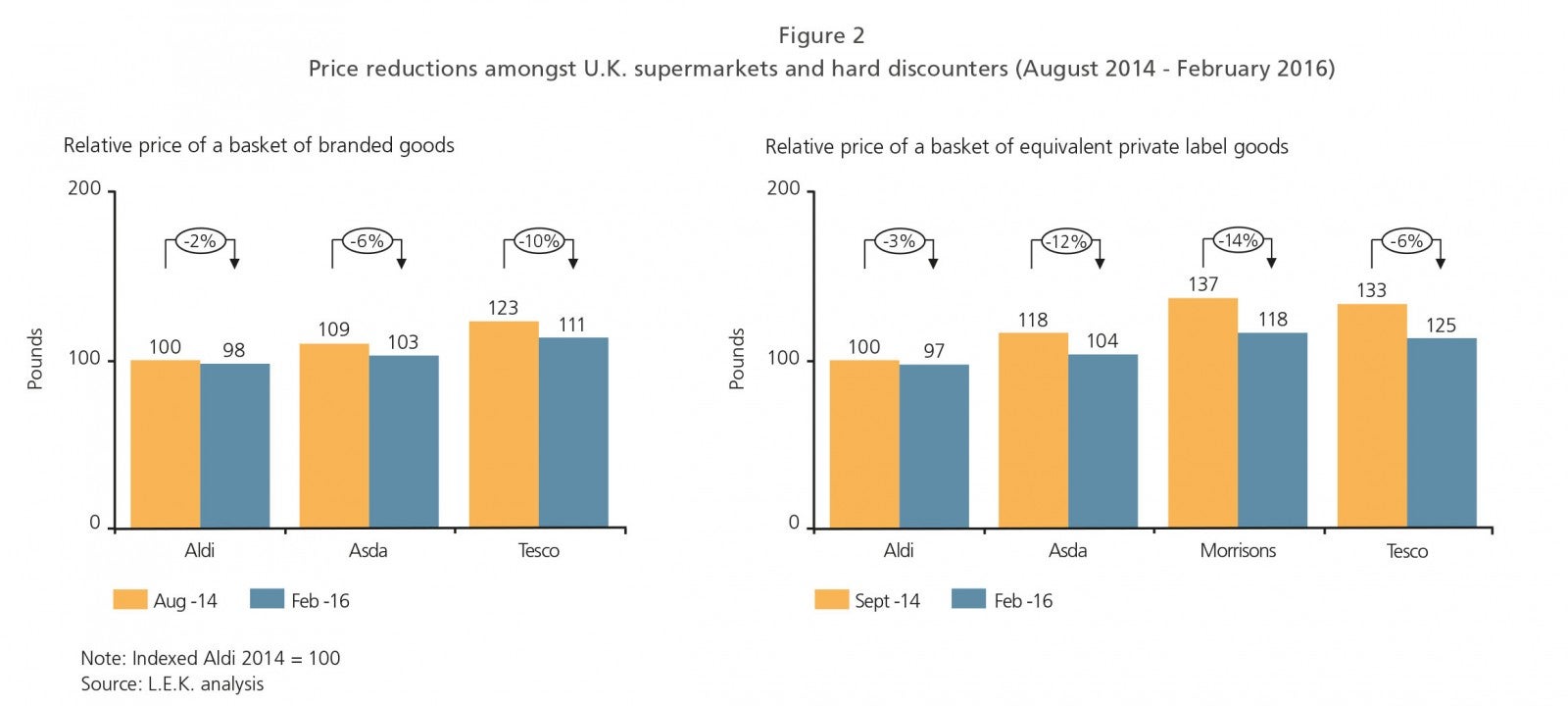

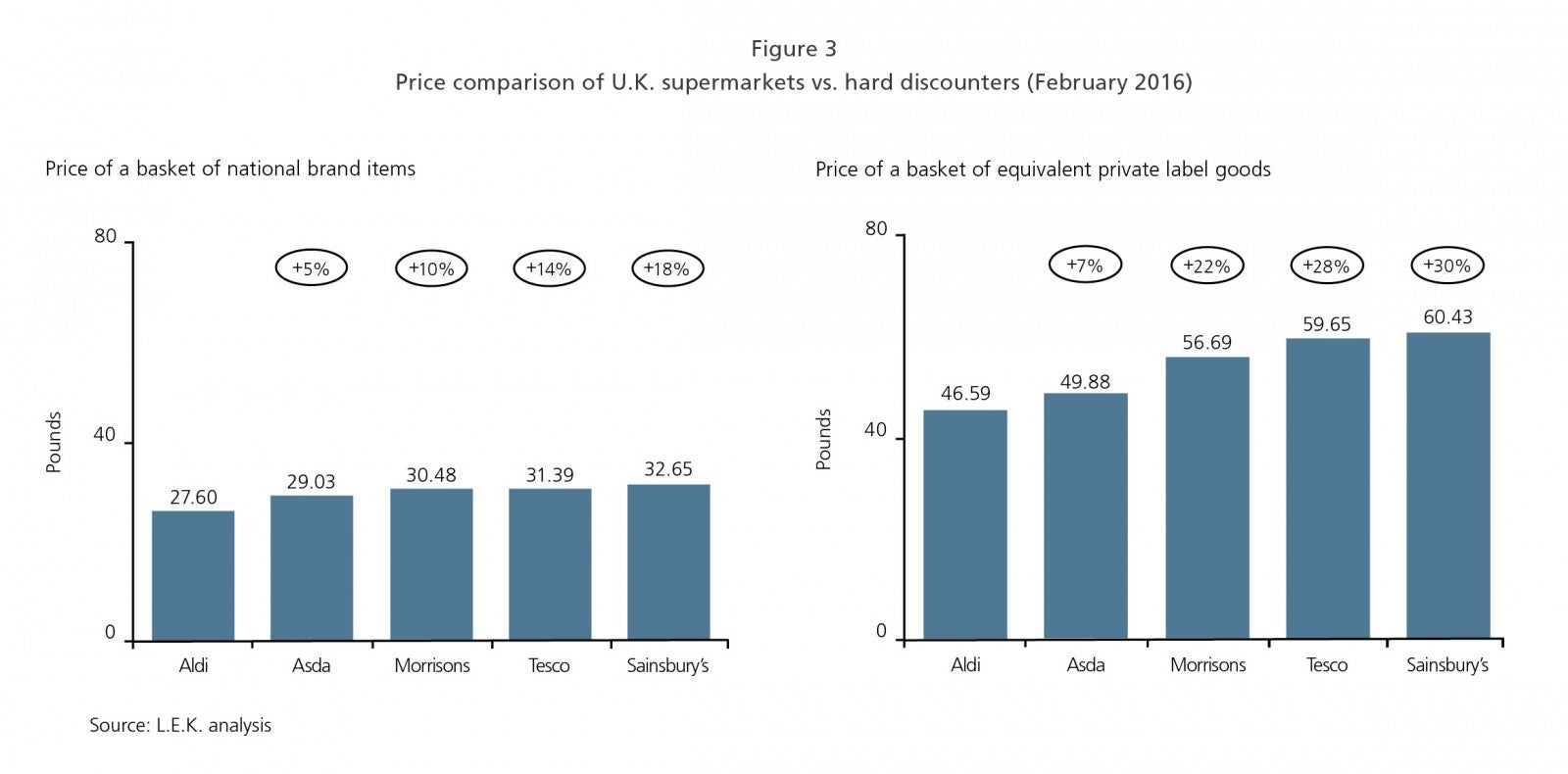

While the big four have certainly made progress since late 2014, our analysis demonstrates that U.K. supermarkets still have a long way to go to regain their leadership. In this paper, L.E.K. reiterates the six key initiatives needed to pass efficiency gains to consumers through lower pricing while ensuring profit protection and an eventual return to growth.

Our first Executive Insights on this topic – “Beating Back Hard Discounters: Lessons from France for the U.K.’s Big Four Supermarkets” – explained how the French supermarkets adopted these initiatives and were able to successfully seize back the market.

Sample Visuals

01222019150150