Summary

It’s been more than three decades since U.S. deregulation spurred the first crop of airline business model innovations. As markets liberalized across the globe, industry reformers searched for sustainable competitive advantage across many different models covering the gamut of service level, aircraft gauge, geography, frequency and price.

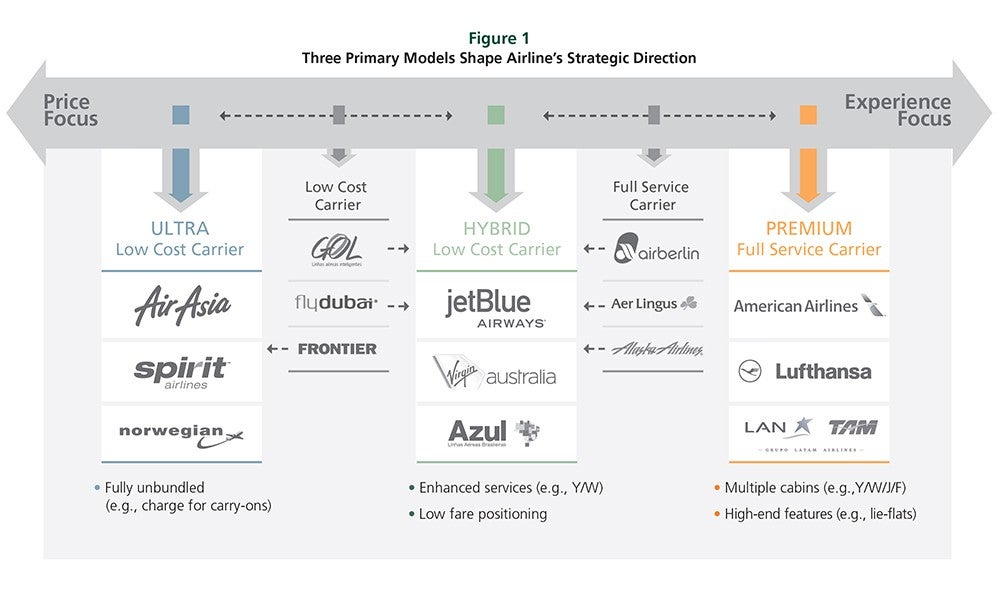

What developed over the 2000s was a clear dichotomy between traditional full-service carriers (FSCs) and upstart low-cost carriers (LCCs). Against this backdrop, L.E.K. Consulting examines a market that is evolving toward three primary business models.

Sample Visuals

02142018170231